A legal title establishes your official ownership of a property, providing the documented evidence needed to prove your rights against any disputes. Understanding the implications of legal title can protect your investment and ensure clear transfer during sales or inheritance. Explore the rest of this article to fully grasp how legal title impacts your property rights and transactions.

Table of Comparison

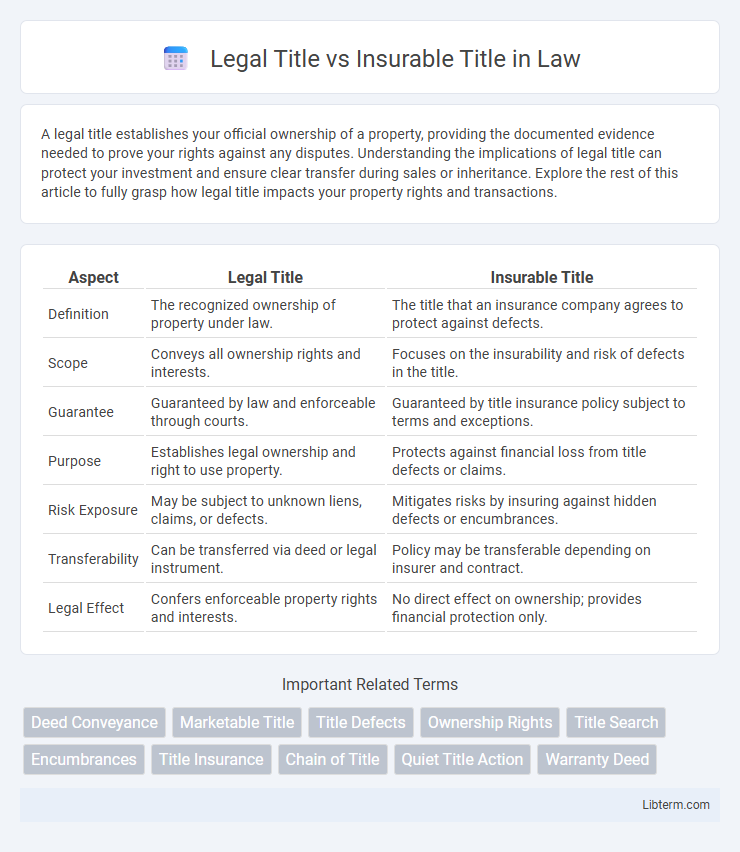

| Aspect | Legal Title | Insurable Title |

|---|---|---|

| Definition | The recognized ownership of property under law. | The title that an insurance company agrees to protect against defects. |

| Scope | Conveys all ownership rights and interests. | Focuses on the insurability and risk of defects in the title. |

| Guarantee | Guaranteed by law and enforceable through courts. | Guaranteed by title insurance policy subject to terms and exceptions. |

| Purpose | Establishes legal ownership and right to use property. | Protects against financial loss from title defects or claims. |

| Risk Exposure | May be subject to unknown liens, claims, or defects. | Mitigates risks by insuring against hidden defects or encumbrances. |

| Transferability | Can be transferred via deed or legal instrument. | Policy may be transferable depending on insurer and contract. |

| Legal Effect | Confers enforceable property rights and interests. | No direct effect on ownership; provides financial protection only. |

Understanding Legal Title: Definition and Importance

Legal title refers to the formal ownership recognized by law, granting the holder the right to control, use, and transfer property. It is essential for establishing clear ownership and protecting against disputes during transactions, ensuring the holder's authority over the asset. Understanding legal title is crucial for buyers, lenders, and insurers to verify rightful ownership and secure property interests.

What is Insurable Title? Key Concepts Explained

Insurable title refers to a property ownership status that is protected by a title insurance policy against defects, liens, or claims that may not be apparent in public records. Unlike legal title, which establishes formal ownership rights recognized by law, insurable title focuses on the assurance of clear ownership and marketability, minimizing financial risk for buyers and lenders. This concept ensures that any potential title disputes discovered after purchase will be covered within the policy terms, safeguarding the investment in real estate transactions.

Legal Title vs Insurable Title: Main Differences

Legal title refers to the official ownership of a property as recorded in public records, granting the holder full rights and responsibilities under the law. Insurable title, on the other hand, is a title that meets the requirements for title insurance, protecting the buyer or lender against potential defects or disputes that could arise later. The main differences lie in the scope of protection and risk assessment: legal title establishes ownership, while insurable title ensures coverage against hidden defects or claims not found in public records.

Why Legal Title Matters in Real Estate Transactions

Legal title in real estate transactions establishes clear ownership recognized by law, enabling the holder to transfer property rights and secure financing. It matters because without legal title, ownership claims lack enforceability, potentially leading to disputes or loss of property. Insurable title protects against defects unknown at the time of sale, but only legal title provides the authoritative proof of ownership required for legitimate control and use of real estate assets.

The Role of Insurable Title in Property Purchases

Insurable title protects buyers against unknown defects or legal issues not revealed by a legal title search, ensuring financial compensation if title problems arise post-purchase. While legal title confirms ownership through proper documentation and recording, insurable title adds a layer of security by covering risks like fraud, errors, or undisclosed liens. This insurance is crucial in property transactions to safeguard buyers and lenders from potential losses tied to hidden title defects.

Title Insurance: Protecting Against Insurable Title Risks

Title insurance protects property buyers from insurable title risks by covering financial loss due to defects in the insurable title, which may not be evident in the legal title documentation. While legal title confirms ownership rights as recorded, insurable title assesses potential hidden issues like liens, encumbrances, or fraud that could affect ownership claims. This distinction ensures buyers are safeguarded against unforeseen claims, making title insurance essential for secure real estate transactions.

Common Issues Affecting Legal and Insurable Title

Common issues affecting both legal title and insurable title include unresolved liens, boundary disputes, and errors in public records that can cloud ownership. Defects such as forged signatures, undisclosed heirs, and fraudulent transfers often impact the legal title, while insurable title concerns center on risks that insurance policies may exclude, like zoning restrictions or unrecorded easements. Resolving these issues typically requires thorough title searches, legal documentation, and insurance underwriting to ensure clear ownership and protection against potential claims.

Resolving Title Defects: Steps and Solutions

Resolving title defects requires a thorough title search and obtaining a clear legal title, which proves rightful ownership recognized by law through documented chain of ownership and absence of liens. Insurable title, ensured by title insurance, protects against potential undiscovered defects by covering losses from claims such as errors in public records, forgery, or unknown heirs. Key solutions include conducting a title cure process, obtaining title insurance policies, and working with title companies or attorneys to address encumbrances, quitclaim deeds, or corrective legal actions for a marketable, insurable property title.

How Lenders View Legal vs Insurable Title

Lenders prioritize legal title as it establishes the borrower's official ownership rights, ensuring clear authority to use the property as collateral. Insurable title offers protection against potential defects or claims that could affect ownership but does not replace the need for legal title verification. The combination of legal title confirmation and insurable title insurance provides lenders with comprehensive security in property transactions.

Choosing Between Legal and Insurable Title: Best Practices

Choosing between legal title and insurable title involves evaluating the certainty of ownership versus the protection against undiscovered claims. Best practices recommend obtaining legal title for clear ownership rights, while securing insurable title through title insurance mitigates risks related to defects or liens. Ensuring a thorough title search combined with appropriate insurance safeguards property investments and minimizes potential legal disputes.

Legal Title Infographic