Performance-based budgeting links funding to measurable outcomes, ensuring resources are allocated efficiently to achieve specific goals. This approach enhances transparency and accountability by focusing on results rather than input levels. Explore the rest of the article to understand how performance-based budgeting can transform your organization's financial planning.

Table of Comparison

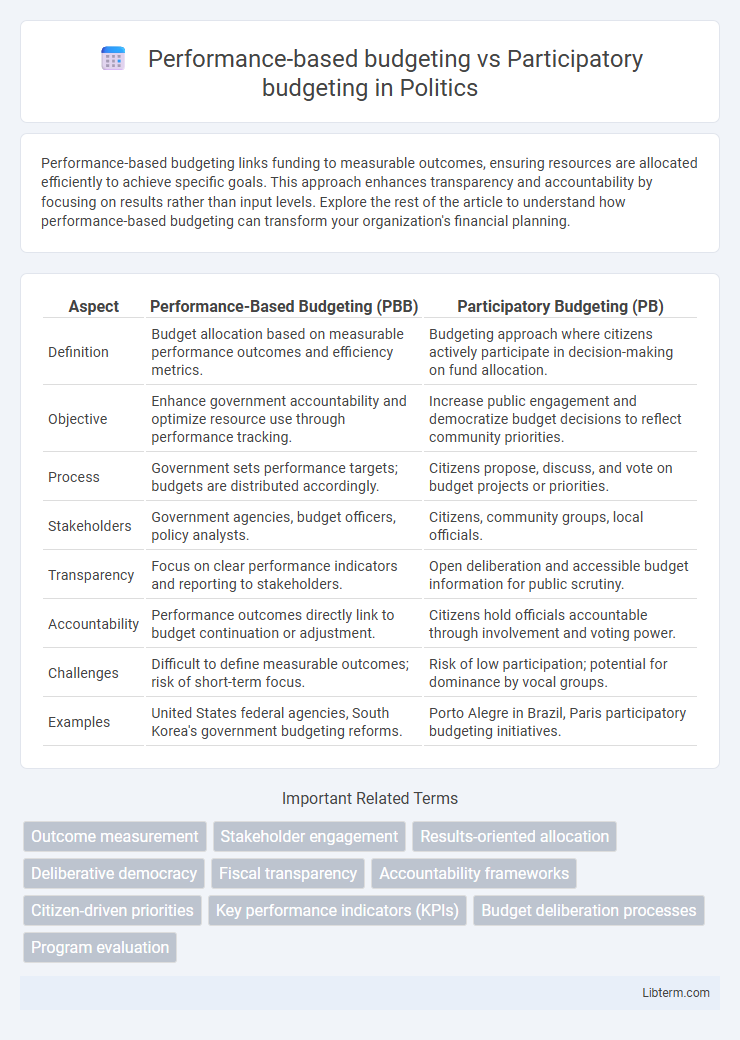

| Aspect | Performance-Based Budgeting (PBB) | Participatory Budgeting (PB) |

|---|---|---|

| Definition | Budget allocation based on measurable performance outcomes and efficiency metrics. | Budgeting approach where citizens actively participate in decision-making on fund allocation. |

| Objective | Enhance government accountability and optimize resource use through performance tracking. | Increase public engagement and democratize budget decisions to reflect community priorities. |

| Process | Government sets performance targets; budgets are distributed accordingly. | Citizens propose, discuss, and vote on budget projects or priorities. |

| Stakeholders | Government agencies, budget officers, policy analysts. | Citizens, community groups, local officials. |

| Transparency | Focus on clear performance indicators and reporting to stakeholders. | Open deliberation and accessible budget information for public scrutiny. |

| Accountability | Performance outcomes directly link to budget continuation or adjustment. | Citizens hold officials accountable through involvement and voting power. |

| Challenges | Difficult to define measurable outcomes; risk of short-term focus. | Risk of low participation; potential for dominance by vocal groups. |

| Examples | United States federal agencies, South Korea's government budgeting reforms. | Porto Alegre in Brazil, Paris participatory budgeting initiatives. |

Understanding Performance-Based Budgeting

Performance-based budgeting allocates funds based on measurable outcomes, enhancing accountability and ensuring resources directly support strategic goals. This method links financial inputs to program outputs and impacts, facilitating data-driven decision-making and efficient resource management. Understanding performance-based budgeting enables governments and organizations to prioritize projects that demonstrate tangible results and improved public service delivery.

Defining Participatory Budgeting

Participatory budgeting is a democratic process in which community members directly decide how to allocate a portion of a public budget, enhancing transparency and citizen engagement. Unlike performance-based budgeting, which allocates funds based on program outcomes and efficiency metrics, participatory budgeting emphasizes inclusivity and collective decision-making. This approach fosters local empowerment by allowing residents to propose and vote on spending priorities, aligning budget allocations with community needs.

Core Principles of Each Approach

Performance-based budgeting centers on allocating resources according to measurable outputs and outcomes, emphasizing efficiency, accountability, and results-driven management. Participatory budgeting prioritizes citizen engagement and democratic involvement, allowing community members to influence budget decisions directly to reflect local needs and priorities. Both methods aim to improve public sector effectiveness but diverge fundamentally in their focus on quantitative performance metrics versus inclusive decision-making processes.

Key Differences Between the Two Methods

Performance-based budgeting emphasizes allocating resources based on measurable outcomes and efficiency, prioritizing accountability and strategic goal achievement. Participatory budgeting involves community members directly in decision-making, fostering transparency and public engagement in the allocation of funds. The key difference lies in Performance-based budgeting relying on data-driven performance metrics, while Participatory budgeting centers on citizen involvement and democratic participation.

Advantages of Performance-Based Budgeting

Performance-based budgeting enhances resource allocation efficiency by linking funds directly to measurable outcomes and organizational goals. It improves accountability and transparency, enabling policymakers to track program effectiveness and make data-driven decisions. This approach facilitates continuous performance improvement by identifying areas that require adjustments or increased investment.

Strengths of Participatory Budgeting

Participatory budgeting empowers citizens by directly involving them in decision-making processes, enhancing transparency and accountability in public fund allocation. This approach fosters community engagement, improves trust in government institutions, and ensures that budget priorities align closely with local needs and preferences. Such inclusive participation often leads to more equitable resource distribution and increased public satisfaction with budget outcomes.

Challenges and Limitations of Each Model

Performance-based budgeting faces challenges such as difficulty in accurately measuring outcomes, data collection constraints, and potential neglect of qualitative benefits, leading to an incomplete assessment of program effectiveness. Participatory budgeting encounters limitations including limited citizen engagement, representation biases, resource-intensive processes, and potential conflicts between stakeholder interests, which can hinder equitable decision-making. Both models struggle with balancing transparency, accountability, and the practical complexities of budget implementation within diverse governance contexts.

Impact on Transparency and Accountability

Performance-based budgeting enhances transparency by linking financial allocations directly to measurable outcomes, enabling stakeholders to assess government efficiency and results. Participatory budgeting increases accountability by involving citizens in decision-making processes, fostering greater public oversight and trust in resource distribution. Both approaches improve governmental transparency and accountability through complementary mechanisms of data-driven evaluation and community engagement.

Case Studies: Real-World Applications

Performance-based budgeting in the United States' defense sector demonstrated significant improvements in resource allocation by linking expenditures to measurable outcomes, enhancing accountability and efficiency. Participatory budgeting in Porto Alegre, Brazil, empowered citizens to directly influence local government spending, resulting in increased transparency and community-driven development projects. Both budgeting approaches showcase distinct real-world applications where performance-based budgeting prioritizes outcome optimization, while participatory budgeting fosters civic engagement and consensus-based financial decisions.

Choosing the Right Budgeting Approach for Your Organization

Performance-based budgeting allocates resources based on measurable outcomes and efficiency metrics, making it ideal for organizations aiming to enhance accountability and align spending with strategic goals. Participatory budgeting engages stakeholders directly in decision-making, fostering transparency and community involvement, which suits organizations prioritizing democratic processes and social equity. Selecting the right budgeting approach depends on your organization's objectives, whether optimizing performance metrics or promoting inclusive participation.

Performance-based budgeting Infographic