Partial distribution refers to the allocation of products or services to selected locations or markets rather than full-scale distribution. This strategy helps businesses focus on target areas, manage resources efficiently, and tailor marketing efforts to specific customer segments. Explore the rest of the article to understand how partial distribution can optimize Your supply chain and boost market presence.

Table of Comparison

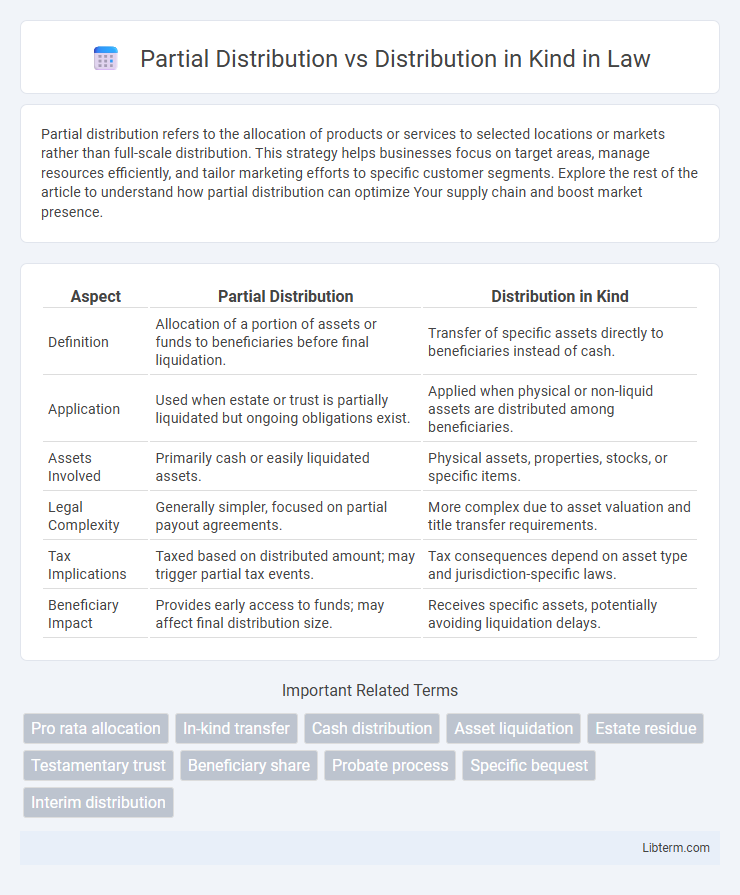

| Aspect | Partial Distribution | Distribution in Kind |

|---|---|---|

| Definition | Allocation of a portion of assets or funds to beneficiaries before final liquidation. | Transfer of specific assets directly to beneficiaries instead of cash. |

| Application | Used when estate or trust is partially liquidated but ongoing obligations exist. | Applied when physical or non-liquid assets are distributed among beneficiaries. |

| Assets Involved | Primarily cash or easily liquidated assets. | Physical assets, properties, stocks, or specific items. |

| Legal Complexity | Generally simpler, focused on partial payout agreements. | More complex due to asset valuation and title transfer requirements. |

| Tax Implications | Taxed based on distributed amount; may trigger partial tax events. | Tax consequences depend on asset type and jurisdiction-specific laws. |

| Beneficiary Impact | Provides early access to funds; may affect final distribution size. | Receives specific assets, potentially avoiding liquidation delays. |

Introduction to Distribution Methods

Partial distribution distributes a portion of an estate or assets to beneficiaries, often used to provide immediate relief or manage liquidity constraints, while full distribution in kind transfers the entire estate's assets directly without converting them to cash. Distribution methods vary based on legal frameworks, asset types, and beneficiary needs, with partial distribution enabling phased allocation and distribution in kind requiring precise valuation and agreement among heirs. Understanding these core differences optimizes estate settlement processes and ensures equitable asset transfer aligned with testamentary intentions.

Definition of Distribution in Kind

Distribution in kind refers to the process of allocating assets or property directly to shareholders or beneficiaries instead of cash payments, typically occurring during dividend disbursements or liquidation events. This method involves transferring physical assets, such as shares, real estate, or inventory, proportionally according to ownership stakes. It contrasts with partial distribution, which may include a combination of cash and asset transfers or distributions made incrementally rather than as a whole.

Definition of Partial Distribution

Partial distribution refers to the disbursement of only a portion of an estate or asset to beneficiaries, where the full distribution is not completed at once, often due to the need for further asset valuation or debt settlement. Distribution in kind involves the allocation of specific assets or property directly to beneficiaries, rather than converting the estate into cash prior to distribution. Partial distribution allows for incremental transfer of assets, facilitating liquidity management and creditor claims handling within estate administration.

Key Differences Between Partial and In-Kind Distribution

Partial distribution involves transferring a portion of assets or funds to beneficiaries, whereas distribution in kind refers to transferring specific physical assets instead of cash. Key differences include liquidity impact, as partial distributions often involve cash or liquid assets, while in-kind distributions maintain asset ownership without liquidation. Tax implications also vary, with in-kind distributions potentially triggering capital gains based on asset valuation at the time of transfer.

Legal Implications of Each Method

Partial distribution involves allocating a portion of assets to shareholders while retaining the remainder within the company, which can affect shareholder rights and trigger specific regulatory requirements under corporate law. Distribution in kind entails transferring assets other than cash directly to shareholders, often necessitating thorough valuation to comply with tax regulations and avoid disputes over asset liquidity and fairness. Legal implications of distribution in kind also include potential impacts on creditor protection, as tangible asset distributions may alter the company's balance sheet and solvency status more significantly than partial cash distributions.

Tax Considerations for Beneficiaries

Partial distribution involves transferring a portion of trust assets to beneficiaries, triggering taxable income only on the distributed amount, while distributions in kind transfer assets without liquidation, potentially deferring capital gains taxes. Beneficiaries receiving partial distributions must report income based on the fair market value of the cash or property received, whereas in-kind distributions require careful valuation to determine any taxable gain or loss. Tax-efficient planning leverages distributions in kind to minimize immediate tax liability, but beneficiaries must be aware of basis adjustments and potential future capital gains upon asset sale.

Common Scenarios for Partial Distribution

Partial distribution occurs when a corporation distributes only a portion of its assets or earnings to shareholders, commonly seen during interim dividend payments or liquidation phases. This approach allows companies to manage cash flow effectively while providing shareholders with periodic returns, unlike full distribution, which involves distributing all remaining assets during complete liquidation. Typical scenarios for partial distribution include spin-offs, recapitalizations, or when a company retains earnings for growth but still rewards shareholders with a dividend.

Advantages and Disadvantages of Distribution in Kind

Distribution in kind allows shareholders to receive assets directly, often resulting in tax deferral as no immediate sale occurs, preserving company liquidity and offering a tangible asset transfer. However, it may cause complexity in asset valuation, potential liquidity issues for recipients, and administrative challenges in asset division. Partial distribution combines cash and asset transfers, balancing liquidity with direct asset benefits, but can complicate tax reporting and shareholder equity adjustments.

Practical Steps in Executing Both Methods

Partial distribution involves allocating a portion of assets to beneficiaries, requiring precise valuation and proportional division based on ownership shares or agreements. Distribution in kind entails transferring specific assets directly to beneficiaries, necessitating detailed asset identification, appraisal, and legally documented transfer to avoid disputes. Both methods demand careful coordination with financial advisors, clear communication with beneficiaries, and adherence to legal and tax regulations to ensure seamless execution.

Choosing the Right Distribution Approach

Choosing between partial distribution and distribution in kind depends on the specific asset types, creditor preferences, and legal framework governing the bankruptcy or insolvency process. Partial distribution typically involves a cash payout to creditors based on available funds, optimizing liquidity and administrative simplicity, whereas distribution in kind allocates physical assets or securities directly, often preferred when asset values are volatile or when preserving entity continuity is critical. Assessing creditor claims, asset liquidity, and potential tax implications ensures the selection of the most efficient and equitable distribution approach for maximizing recovery and satisfying stakeholder interests.

Partial Distribution Infographic