Representative budgeting involves allocating funds based on the needs and preferences of a specific group or community to ensure resources directly support their priorities. This approach enhances transparency and accountability by allowing stakeholders to participate actively in financial decisions. Explore the rest of the article to understand how representative budgeting can transform your organization's financial planning.

Table of Comparison

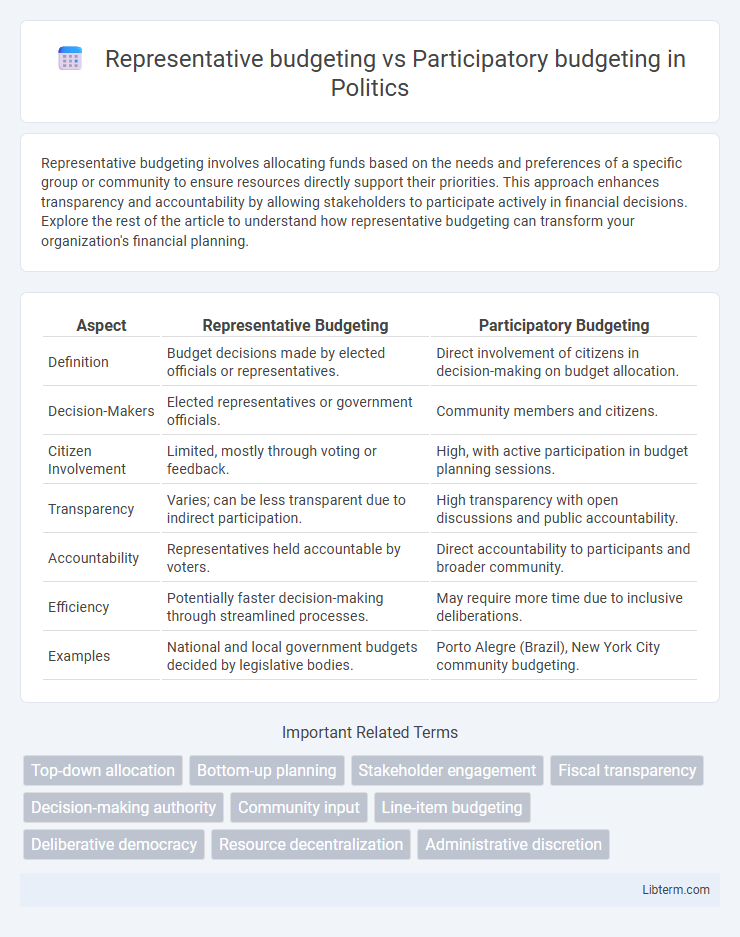

| Aspect | Representative Budgeting | Participatory Budgeting |

|---|---|---|

| Definition | Budget decisions made by elected officials or representatives. | Direct involvement of citizens in decision-making on budget allocation. |

| Decision-Makers | Elected representatives or government officials. | Community members and citizens. |

| Citizen Involvement | Limited, mostly through voting or feedback. | High, with active participation in budget planning sessions. |

| Transparency | Varies; can be less transparent due to indirect participation. | High transparency with open discussions and public accountability. |

| Accountability | Representatives held accountable by voters. | Direct accountability to participants and broader community. |

| Efficiency | Potentially faster decision-making through streamlined processes. | May require more time due to inclusive deliberations. |

| Examples | National and local government budgets decided by legislative bodies. | Porto Alegre (Brazil), New York City community budgeting. |

Understanding Representative Budgeting

Representative budgeting delegates fiscal decision-making to elected officials who allocate funds based on policy priorities and expert advice, ensuring efficiency in managing public resources. This approach centralizes budget authority within government institutions, relying on representatives to balance competing demands and fiscal constraints effectively. Understanding representative budgeting involves recognizing its emphasis on indirect citizen participation through elected delegates rather than direct involvement in budgetary processes.

Defining Participatory Budgeting

Participatory budgeting is a democratic process that allows community members to directly decide how public funds are allocated, fostering transparency and citizen engagement. Unlike representative budgeting, where elected officials control budget decisions, participatory budgeting empowers residents to propose and vote on projects, ensuring that spending aligns with community needs. This approach enhances accountability and encourages inclusive participation, bridging the gap between government and constituents.

Core Principles: Representative vs Participatory Approaches

Representative budgeting relies on elected officials who make financial decisions on behalf of the community, emphasizing delegation and expertise in managing public funds. Participatory budgeting involves direct citizen engagement, allowing community members to propose and vote on budget allocations, fostering transparency and inclusivity. The core principle of representative budgeting centers on accountability through elected representatives, whereas participatory budgeting prioritizes democratic participation and grassroots involvement.

Historical Background of Budgeting Models

Representative budgeting originated in the early 20th century as governments formalized financial planning through elected officials responsible for allocating public funds. Participatory budgeting emerged in the late 1980s in Porto Alegre, Brazil, as a grassroots democratic innovation allowing citizens to directly influence budget decisions. These models reflect a shift from centralized, top-down fiscal control to inclusive, bottom-up financial governance, highlighting evolving demands for transparency and public involvement.

Decision-Making Processes Compared

Representative budgeting centralizes decision-making authority in elected officials who allocate funds based on policy priorities and expert recommendations, often resulting in faster yet less inclusive outcomes. Participatory budgeting involves direct citizen involvement in budget decisions, enhancing transparency and community engagement by allowing residents to propose and vote on funding allocations. This collaborative process fosters greater public accountability but can require more time and resources to reach consensus.

Advantages of Representative Budgeting

Representative budgeting offers efficient decision-making by entrusting elected officials with budget allocation, ensuring expert oversight and accountability. It facilitates streamlined processes and quicker implementation of policies, reducing delays often experienced in direct public involvement. This traditional model also provides consistency and stability in fiscal planning, aligning with established governmental frameworks.

Benefits of Participatory Budgeting

Participatory budgeting empowers citizens by directly involving them in decision-making processes, resulting in increased transparency and accountability in public spending. It fosters community engagement, allowing diverse voices to influence funding priorities and better address local needs. This approach enhances trust between government and residents, leading to more equitable resource allocation and improved public satisfaction.

Common Challenges in Each Approach

Representative budgeting often faces challenges like limited public engagement and potential misalignment with community needs due to decision-making concentrated among elected officials. Participatory budgeting struggles with inclusivity barriers, such as ensuring diverse demographic involvement and managing the complexity of integrating public input into formal budget processes. Both approaches require balancing transparency, accountability, and efficient resource allocation to effectively address diverse stakeholder interests.

Real-World Examples and Case Studies

Representative budgeting is exemplified by the United States federal budget process, where elected officials allocate funds based on macroeconomic priorities and political negotiations, often reflecting national-level policy goals. Participatory budgeting has been effectively implemented in Porto Alegre, Brazil, empowering citizens to directly decide on municipal budget priorities, resulting in increased transparency and improved public service delivery. Case studies from Paris illustrate how participatory budgeting can coexist with traditional models, enhancing citizen engagement without replacing representative decision-making structures.

Choosing the Right Model for Effective Governance

Representative budgeting delegates financial decision-making to elected officials, ensuring streamlined governance but potentially limiting direct citizen influence. Participatory budgeting engages community members in allocating public funds, promoting transparency and enhanced civic involvement. Selecting the right model depends on governance goals, the degree of public engagement desired, and the capacity for administrative support to balance efficiency with inclusivity.

Representative budgeting Infographic