A production center plays a crucial role in streamlining manufacturing processes by centralizing operations, improving efficiency, and reducing costs. It integrates advanced technologies and skilled labor to ensure high-quality output and timely delivery. Discover how optimizing your production center can transform your business by reading the rest of the article.

Table of Comparison

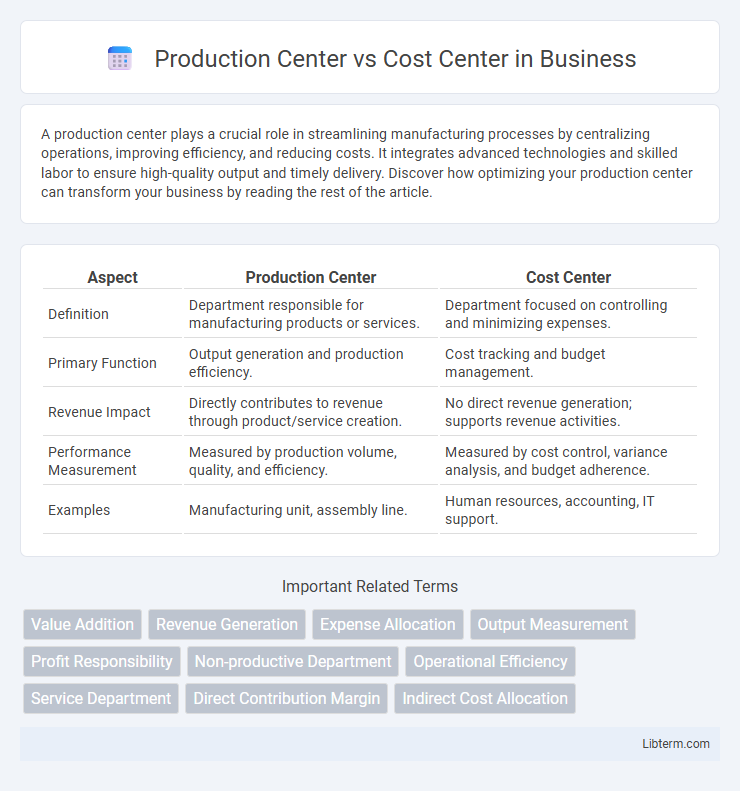

| Aspect | Production Center | Cost Center |

|---|---|---|

| Definition | Department responsible for manufacturing products or services. | Department focused on controlling and minimizing expenses. |

| Primary Function | Output generation and production efficiency. | Cost tracking and budget management. |

| Revenue Impact | Directly contributes to revenue through product/service creation. | No direct revenue generation; supports revenue activities. |

| Performance Measurement | Measured by production volume, quality, and efficiency. | Measured by cost control, variance analysis, and budget adherence. |

| Examples | Manufacturing unit, assembly line. | Human resources, accounting, IT support. |

Introduction to Production Centers and Cost Centers

Production centers are operational units within a company where actual manufacturing or production activities occur, directly contributing to the creation of goods or services. Cost centers, by contrast, are departments or functions that incur costs but do not directly generate revenue, focusing on supporting the production process or overall business operations. Understanding the distinction between production centers and cost centers is essential for accurate cost allocation, budgeting, and performance evaluation in managerial accounting.

Definition of Production Center

A Production Center is a unit within a manufacturing or service organization responsible for the transformation of raw materials into finished goods or services. It focuses on value-added activities that directly contribute to output and revenue generation. Unlike a Cost Center, which only tracks expenses without producing direct output, a Production Center integrates both operational efficiency and quality control to optimize productivity.

Definition of Cost Center

A cost center is a department or unit within an organization responsible solely for incurring costs without directly generating revenue, focusing on controlling and minimizing expenses. Unlike production centers, which are directly involved in manufacturing goods or delivering services, cost centers support operational activities such as administration, maintenance, and quality control. Effective management of cost centers enables organizations to optimize budget allocation and improve overall financial performance.

Key Differences Between Production and Cost Centers

Production centers are primarily responsible for manufacturing goods and directly contribute to revenue generation by transforming raw materials into finished products. Cost centers focus on controlling and minimizing expenses without directly producing output, serving as support units such as maintenance or administration. The key differences lie in their roles: production centers impact profit through output volume, while cost centers influence profitability by managing operational costs efficiently.

Role of Production Centers in Organizations

Production centers play a critical role in organizations by directly contributing to the creation of goods and services, driving revenue generation and operational efficiency. They are responsible for managing resources, overseeing manufacturing processes, and ensuring quality control to meet production targets within budget constraints. Unlike cost centers that focus primarily on controlling expenses without generating revenue, production centers balance cost management with output optimization to achieve strategic business goals.

Role of Cost Centers in Organizations

Cost centers play a critical role in organizations by managing and controlling expenses without directly generating revenue, focusing on efficiency and budget adherence. Unlike production centers, which are responsible for creating goods or services, cost centers provide essential support functions such as human resources, IT, and maintenance. Their performance is measured through cost control metrics and operational effectiveness, enabling better resource allocation and financial accountability.

Impact on Financial Reporting

Production centers directly influence financial reporting by generating revenue and incurring costs tied to manufacturing goods, thereby impacting gross profit and inventory valuation. Cost centers, lacking revenue generation, affect financial statements primarily through expense tracking and control, influencing operating expenses and overall profitability analysis. Accurate allocation of overheads between production and cost centers is crucial for precise product costing and financial transparency.

Performance Measurement and Evaluation

Performance measurement in a Production Center emphasizes efficiency, output quality, and adherence to production schedules, leveraging metrics like units produced, defect rates, and machine uptime. In contrast, Cost Center evaluation prioritizes budget adherence, cost control, and expense variance analysis to optimize resource utilization without directly generating revenue. Both centers use key performance indicators (KPIs) tailored to their operational roles, ensuring targeted management focus on productivity versus cost efficiency.

Advantages and Disadvantages

Production centers enhance operational efficiency by directly contributing to output and revenue generation, but they often incur higher variable costs and require substantial management oversight. Cost centers facilitate tight budget control and expense tracking without the pressure of revenue targets, though they may face challenges in justifying expenditures and demonstrating direct value to the organization. Balancing the strategic focus between production centers' productivity benefits and cost centers' cost containment is critical for optimal resource allocation.

Choosing Between Production Center and Cost Center

Choosing between a production center and a cost center depends on whether the focus is on output generation or expense control within an organization. Production centers are responsible for creating goods or services, directly influencing revenue and operational efficiency, while cost centers primarily track and manage expenditures to optimize budgeting without directly generating income. Evaluating organizational goals, resource allocation, and performance metrics helps determine the appropriate center type for effective management and financial oversight.

Production Center Infographic