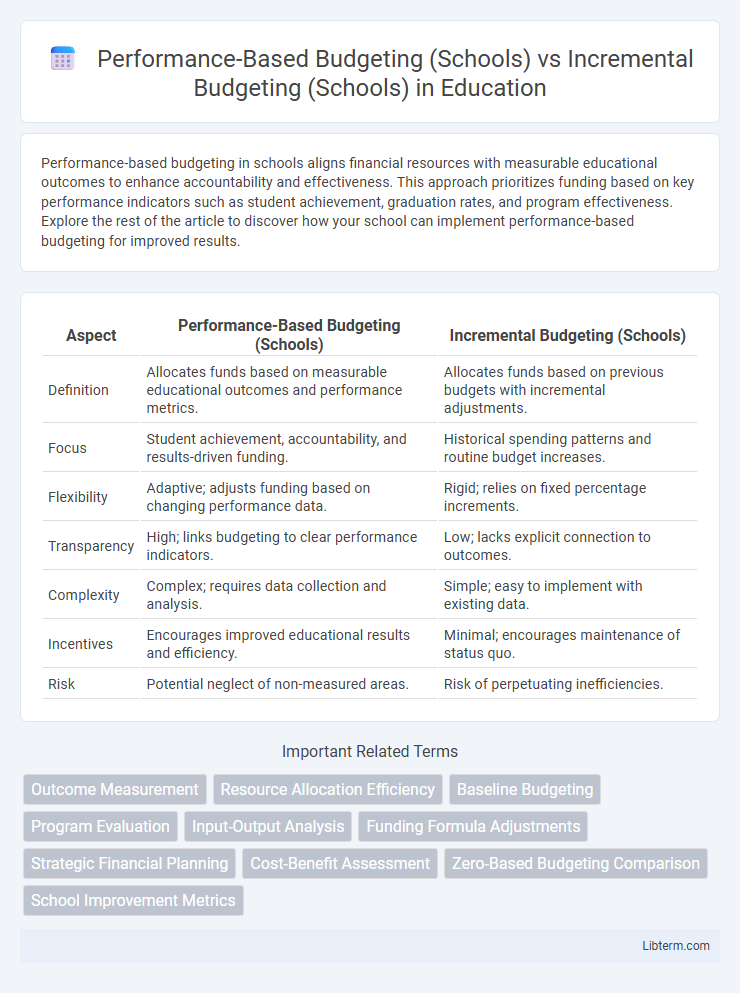

Performance-based budgeting in schools aligns financial resources with measurable educational outcomes to enhance accountability and effectiveness. This approach prioritizes funding based on key performance indicators such as student achievement, graduation rates, and program effectiveness. Explore the rest of the article to discover how your school can implement performance-based budgeting for improved results.

Table of Comparison

| Aspect | Performance-Based Budgeting (Schools) | Incremental Budgeting (Schools) |

|---|---|---|

| Definition | Allocates funds based on measurable educational outcomes and performance metrics. | Allocates funds based on previous budgets with incremental adjustments. |

| Focus | Student achievement, accountability, and results-driven funding. | Historical spending patterns and routine budget increases. |

| Flexibility | Adaptive; adjusts funding based on changing performance data. | Rigid; relies on fixed percentage increments. |

| Transparency | High; links budgeting to clear performance indicators. | Low; lacks explicit connection to outcomes. |

| Complexity | Complex; requires data collection and analysis. | Simple; easy to implement with existing data. |

| Incentives | Encourages improved educational results and efficiency. | Minimal; encourages maintenance of status quo. |

| Risk | Potential neglect of non-measured areas. | Risk of perpetuating inefficiencies. |

Introduction to School Budgeting Approaches

Performance-based budgeting in schools allocates funds based on specific outcomes such as student achievement and graduation rates, emphasizing accountability and resource optimization. Incremental budgeting relies on previous years' budgets with incremental adjustments, offering simplicity but potentially perpetuating inefficiencies and limiting responsiveness to changing educational needs. These contrasting approaches influence how schools prioritize spending, measure success, and adapt to evolving demands in the education sector.

Defining Performance-Based Budgeting in Schools

Performance-Based Budgeting in schools allocates funds based on measurable student outcomes, such as graduation rates, test scores, and attendance, ensuring resources directly support educational goals. Unlike Incremental Budgeting, which adjusts previous budgets by fixed percentages, performance-based systems prioritize efficiency and accountability by linking financial decisions to performance metrics. This approach promotes targeted investments that drive improvements in teaching quality and student achievement.

Overview of Incremental Budgeting in Educational Institutions

Incremental budgeting in educational institutions involves adjusting previous budgets by a fixed percentage to allocate funds for the new fiscal period, emphasizing simplicity and stability. This method maintains established funding patterns, ensuring predictable resource distribution but often limiting flexibility and responsiveness to changing educational needs. Schools using incremental budgeting may struggle to reallocate funds effectively for innovative programs or shifting priorities compared to performance-based budgeting approaches.

Key Differences Between Performance-Based and Incremental Budgeting

Performance-Based Budgeting in schools allocates funds based on specific educational outcomes and measurable results like student achievement and graduation rates, emphasizing accountability and resource efficiency. Incremental Budgeting relies on historical budgets with incremental adjustments, focusing on past spending patterns rather than performance metrics, often leading to less flexibility in addressing current educational needs. The key difference lies in Performance-Based Budgeting's outcome-driven approach versus Incremental Budgeting's reliance on tradition and incremental changes, impacting strategic resource allocation and school improvement initiatives.

Advantages of Performance-Based Budgeting for Schools

Performance-Based Budgeting in schools enhances resource allocation by linking funds directly to student outcomes and program effectiveness, promoting accountability and improved educational results. This approach allows for data-driven decisions that target underperforming areas and optimize the impact of each dollar spent, unlike Incremental Budgeting, which often perpetuates past inefficiencies by adjusting previous budgets with minimal evaluation. By emphasizing measurable performance indicators, schools can foster continuous improvement and align financial planning with strategic educational goals.

Limitations of Incremental Budgeting in Education

Incremental budgeting in schools often leads to inefficiencies by allocating funds based on previous expenditures without considering current educational needs or outcomes. This approach can perpetuate outdated priorities and limit the ability to respond to changing student demographics or new pedagogical methods. It fails to promote accountability or performance improvements, unlike performance-based budgeting which ties funding to measurable educational results.

Impact on Resource Allocation and Student Outcomes

Performance-Based Budgeting in schools allocates funds based on measurable student outcomes, driving targeted investments in high-impact programs and improving resource efficiency. Incremental Budgeting relies on previous year's allocations with slight adjustments, often perpetuating inefficiencies and limiting responsiveness to changing educational needs. Schools using Performance-Based Budgeting typically demonstrate enhanced student achievement and better alignment of financial resources with educational goals compared to those using Incremental Budgeting.

Implementation Challenges for Both Budgeting Models

Performance-Based Budgeting in schools faces implementation challenges such as accurately measuring educational outcomes, aligning budget allocations with performance metrics, and securing stakeholder buy-in amid varying priorities. Incremental Budgeting struggles with difficulties in justifying incremental increases, limited flexibility to address changing educational needs, and the risk of perpetuating inefficiencies without comprehensive review. Both models require robust data systems and transparent communication to overcome resistance and ensure effective resource allocation.

Case Studies: Performance-Based vs Incremental Budgeting in Schools

Case studies of Performance-Based Budgeting (PBB) in schools reveal enhanced resource allocation tied to measurable student outcomes, leading to improved academic performance and accountability. In contrast, Incremental Budgeting often perpetuates previous funding patterns with minimal adjustments, resulting in less flexibility and slower response to changing educational needs. Comparative analyses highlight that PBB schools demonstrate greater efficiency and targeted investment in programs directly impacting student achievement, while Incremental Budgeting schools may struggle with outdated budget structures and limited innovation.

Choosing the Right Budgeting Approach for Your School

Performance-Based Budgeting in schools links resources directly to student outcomes and program effectiveness, promoting accountability and targeted improvements. Incremental Budgeting adjusts previous budgets slightly, favoring stability but risking inefficiency by perpetuating outdated allocations. Choosing the right approach depends on your school's goals: prioritize Performance-Based Budgeting for outcome-driven resource allocation or Incremental Budgeting for simplicity and consistency in financial planning.

Performance-Based Budgeting (Schools) Infographic