An indemnifier assumes responsibility for compensating losses or damages incurred by another party, ensuring financial protection and risk management. This legal role is crucial in contracts where one party agrees to hold another harmless from potential claims or liabilities. Discover how understanding your indemnifier's obligations can safeguard your interests by reading the rest of the article.

Table of Comparison

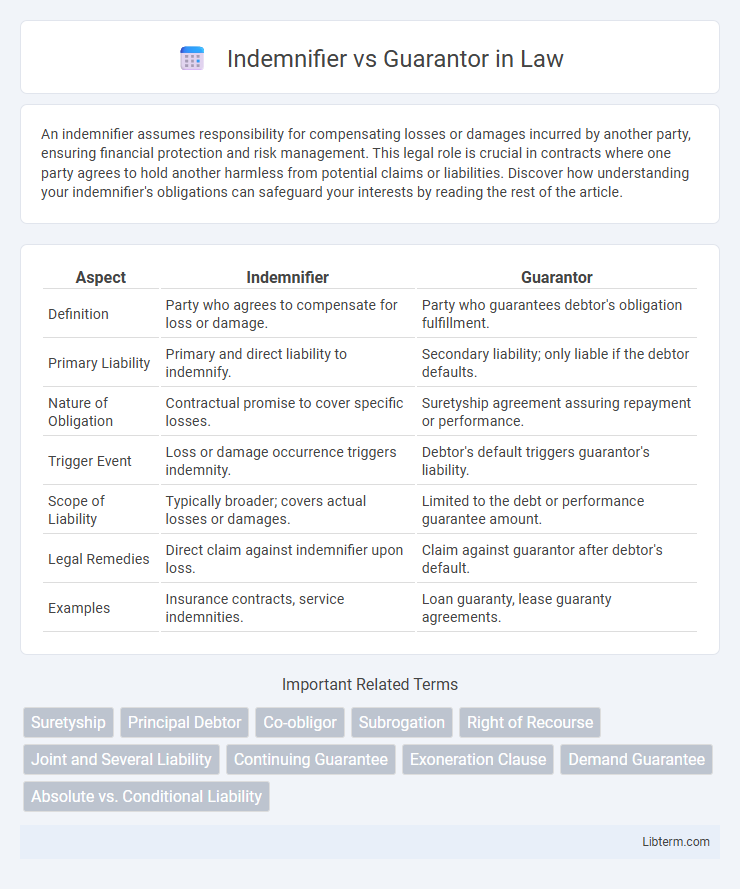

| Aspect | Indemnifier | Guarantor |

|---|---|---|

| Definition | Party who agrees to compensate for loss or damage. | Party who guarantees debtor's obligation fulfillment. |

| Primary Liability | Primary and direct liability to indemnify. | Secondary liability; only liable if the debtor defaults. |

| Nature of Obligation | Contractual promise to cover specific losses. | Suretyship agreement assuring repayment or performance. |

| Trigger Event | Loss or damage occurrence triggers indemnity. | Debtor's default triggers guarantor's liability. |

| Scope of Liability | Typically broader; covers actual losses or damages. | Limited to the debt or performance guarantee amount. |

| Legal Remedies | Direct claim against indemnifier upon loss. | Claim against guarantor after debtor's default. |

| Examples | Insurance contracts, service indemnities. | Loan guaranty, lease guaranty agreements. |

Understanding Indemnifiers and Guarantors

Indemnifiers provide protection by agreeing to compensate for any loss or damage incurred, often assuming primary liability in a contract. Guarantors, on the other hand, offer secondary liability, stepping in only if the principal party fails to fulfill their obligations. Understanding these roles is crucial for risk management and contractual clarity in financial and legal agreements.

Key Definitions: Indemnity vs Guarantee

Indemnity involves one party promising to compensate another for any loss or damage incurred, ensuring full reimbursement without requiring the creditor to take action against a third party. Guarantee is a secondary obligation where the guarantor promises to fulfill the debtor's obligation only if the debtor defaults, making it a conditional liability. Key distinctions include indemnity being a primary liability with immediate compensation responsibility, while guarantee depends on the debtor's failure to perform.

Legal Framework: Indemnifiers and Guarantors

Indemnifiers assume primary liability to compensate for loss or damage under contract, while guarantors provide secondary liability, stepping in only if the principal debtor defaults. The legal framework governing indemnifiers is typically more straightforward, as their obligation arises immediately upon breach without requiring creditor action against the principal. Guarantor obligations are governed by specific statutes and common law principles, often imposing stricter requirements such as the necessity of a signed written agreement and careful interpretation of the terms to enforce suretyship.

Primary Obligations: Who Bears the Risk?

An indemnifier assumes primary liability by agreeing to compensate for specific losses or damages without requiring the creditor to exhaust remedies against the principal debtor first. In contrast, a guarantor's obligation is secondary, activating only if the principal debtor defaults, thus bearing risk contingent upon default occurrence. Understanding this distinction clarifies who bears the financial burden initially, with the indemnifier facing immediate exposure and the guarantor serving as a backup risk bearer.

Nature of Liability: Conditional vs Unconditional

An indemnifier's liability is unconditional, meaning they must fulfill their obligation regardless of the debtor's default or other conditions. A guarantor's liability is conditional, activated only when the primary debtor fails to meet the payment or performance obligations. This fundamental distinction impacts risk exposure and the enforcement process in financial and legal agreements.

Rights and Remedies of Parties Involved

Indemnifiers have the primary right to seek compensation from the indemnified party for losses specified in the indemnity agreement, while guarantors' rights are contingent upon the debtor's default and usually allow them to enforce payment guarantees after exhaustion of the principal obligor's assets. Remedies for indemnifiers typically include direct claims for recovery and defense against third-party claims, whereas guarantors may pursue subrogation rights to step into the creditor's shoes post-payment. Both parties must navigate contractual terms that define the scope and limits of indemnity or guarantee, influencing enforcement strategies and risk exposure.

Termination and Discharge of Liabilities

Termination and discharge of liabilities differ significantly between indemnifiers and guarantors, with indemnifiers typically being discharged once the indemnity obligation is fulfilled or the risk event causing liability ends. Guarantors, however, are discharged when the principal debtor's liability is lawfully terminated, including through payment, release, or novation. Courts often scrutinize any agreement modifying the principal contract to avoid unintentionally releasing guarantors from their obligations.

Differences in Enforcement Procedures

Indemnifiers are directly liable from the moment a loss arises, allowing the obligee to claim compensation immediately without first pursuing the principal debtor. Guarantors, in contrast, are secondary obligors and can only be compelled to pay after the principal debtor defaults and enforcement actions against the principal are unsuccessful. Enforcement procedures for indemnifiers are typically more straightforward, whereas guarantors benefit from procedural protections such as the requirement for the creditor to exhaust remedies against the principal before proceeding.

Practical Examples in Business and Law

An indemnifier in business agreements assumes direct responsibility to compensate for losses or damages, such as a contractor agreeing to indemnify a client against property damage during a project. A guarantor provides a secondary assurance, often backing a borrower's loan repayment to a lender if the primary debtor defaults. Legal cases often highlight the difference where an indemnifier faces immediate liability upon a claim, while a guarantor's obligation arises only after the primary party fails to fulfill their duty.

Choosing Between an Indemnifier or Guarantor

Choosing between an indemnifier and a guarantor depends on the specific risk allocation and financial responsibility desired in the contract. An indemnifier assumes primary liability and must cover losses regardless of the principal debtor's default, while a guarantor provides secondary liability, paying only if the primary debtor defaults. Legal implications and enforcement mechanisms differ, making it essential to evaluate the nature of the obligation and the strength of the financial backing before selecting either party.

Indemnifier Infographic