The characteristic polynomial is a fundamental concept in linear algebra used to determine the eigenvalues of a matrix by evaluating the polynomial derived from the determinant of the matrix minus a scalar multiple of the identity matrix. It plays a crucial role in understanding matrix properties, stability analysis, and systems of differential equations. Explore the rest of the article to deepen your grasp of how the characteristic polynomial influences various mathematical and practical applications.

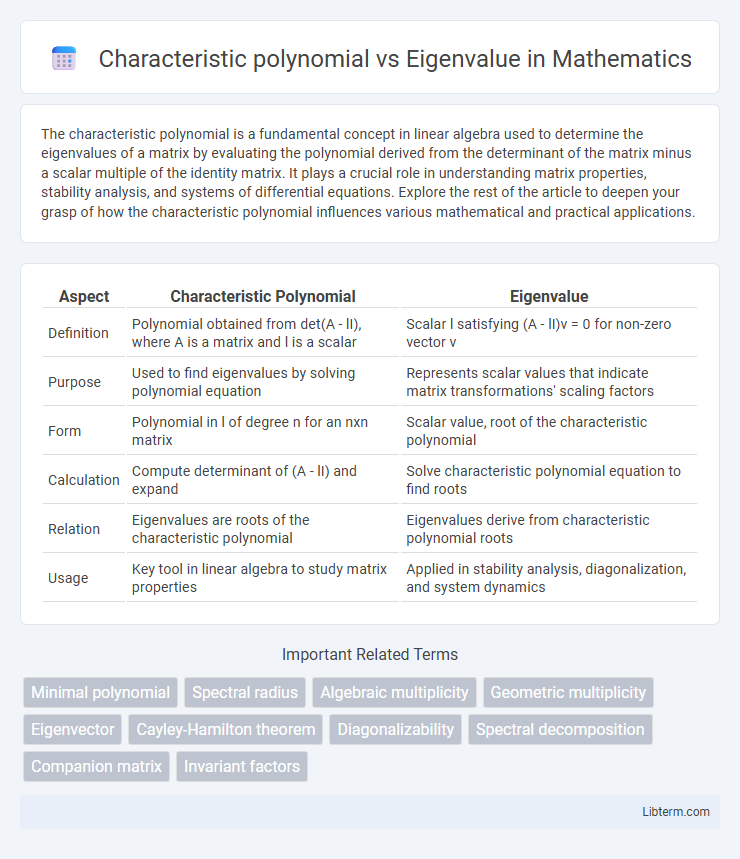

Table of Comparison

| Aspect | Characteristic Polynomial | Eigenvalue |

|---|---|---|

| Definition | Polynomial obtained from det(A - lI), where A is a matrix and l is a scalar | Scalar l satisfying (A - lI)v = 0 for non-zero vector v |

| Purpose | Used to find eigenvalues by solving polynomial equation | Represents scalar values that indicate matrix transformations' scaling factors |

| Form | Polynomial in l of degree n for an nxn matrix | Scalar value, root of the characteristic polynomial |

| Calculation | Compute determinant of (A - lI) and expand | Solve characteristic polynomial equation to find roots |

| Relation | Eigenvalues are roots of the characteristic polynomial | Eigenvalues derive from characteristic polynomial roots |

| Usage | Key tool in linear algebra to study matrix properties | Applied in stability analysis, diagonalization, and system dynamics |

Introduction to Characteristic Polynomial and Eigenvalue

The characteristic polynomial of a square matrix is a fundamental tool in linear algebra, obtained by calculating the determinant of the matrix subtracted by a scalar multiple of the identity matrix. Its roots, known as eigenvalues, reveal critical properties of the matrix, including stability and diagonalizability. Eigenvalues provide insight into matrix transformations, helping to analyze systems in engineering, physics, and data science.

Definitions: Characteristic Polynomial and Eigenvalue

The characteristic polynomial is a polynomial derived from a square matrix A, defined as det(lI - A), where l is a scalar and I is the identity matrix, used to determine the matrix's eigenvalues. An eigenvalue is a scalar l for which there exists a nonzero vector v satisfying the equation Av = lv, indicating that v is an eigenvector corresponding to l. The roots of the characteristic polynomial are precisely the eigenvalues of the matrix, linking these two fundamental concepts in linear algebra.

Mathematical Relationship Between Characteristic Polynomial and Eigenvalues

The characteristic polynomial of a matrix is defined as the determinant of lI minus the matrix, where l represents a scalar variable. The eigenvalues of the matrix are precisely the roots of this characteristic polynomial, satisfying the equation where the polynomial equals zero. This direct relationship allows the eigenvalues to be found by solving the characteristic polynomial equation det(lI - A) = 0.

How to Compute the Characteristic Polynomial of a Matrix

The characteristic polynomial of a matrix is computed by finding the determinant of the matrix subtracted by lambda times the identity matrix, represented as det(A - lI). This polynomial encapsulates key properties of the matrix and its roots correspond to the matrix's eigenvalues. Calculating this determinant, typically through cofactor expansion or row reduction, forms the foundation for identifying eigenvalues and analyzing matrix behavior.

Eigenvalue Calculation: Step-by-Step Process

Eigenvalue calculation begins by forming the characteristic polynomial from the matrix \( A \) as \( \det(A - \lambda I) = 0 \), where \( \lambda \) is the eigenvalue variable and \( I \) is the identity matrix. Solving this polynomial equation yields eigenvalues \( \lambda \) that satisfy the determinant condition. Each eigenvalue corresponds to a non-trivial solution of \( (A - \lambda I)x = 0 \), linking the characteristic polynomial directly to eigenvalue determination.

Importance of Characteristic Polynomial in Linear Algebra

The characteristic polynomial is essential in linear algebra as it provides a systematic method for finding eigenvalues of a matrix, which are the roots of this polynomial. These eigenvalues reveal critical properties of linear transformations such as stability, diagonalizability, and spectral decomposition. Understanding the characteristic polynomial facilitates solving systems of differential equations, analyzing matrix behavior, and determining invariant subspaces.

Applications of Eigenvalues in Real-World Problems

Eigenvalues derived from the characteristic polynomial of a matrix are crucial in diverse real-world applications such as stability analysis in engineering systems, vibrations in mechanical structures, and Google's PageRank algorithm for ranking web pages. In quantum mechanics, eigenvalues determine energy levels of systems, while in finance, they help in portfolio optimization by analyzing covariance matrices. These applications rely on eigenvalues to extract essential system properties, enabling efficient problem-solving and decision-making across disciplines.

Differences Between Characteristic Polynomial and Eigenvalue

The characteristic polynomial is a polynomial derived from a square matrix, defined as the determinant of the matrix subtracted by a scalar times the identity matrix, while an eigenvalue is a scalar that satisfies this polynomial equation. Eigenvalues are the roots of the characteristic polynomial and represent the scalars for which the matrix transformation stretches or compresses vectors without changing their direction. Unlike the characteristic polynomial, which is an algebraic expression, eigenvalues are numerical values that provide crucial information about a matrix's properties such as stability and diagonalizability.

Common Mistakes and Pitfalls in Computation

Characteristic polynomial and eigenvalue computations often suffer from common mistakes such as incorrect polynomial formation due to sign errors or matrix entry misinterpretation. Miscalculating roots of the characteristic polynomial leads to inaccurate eigenvalues, especially when numerical methods or symbolic solvers face precision limits. Neglecting to verify multiplicities and eigenvector consistency further complicates the correct identification of eigenvalues, impacting stability analysis and diagonalization tasks.

Summary: Characteristic Polynomial vs Eigenvalue

The characteristic polynomial of a matrix is a polynomial whose roots are the eigenvalues of that matrix. Eigenvalues represent the scalar values for which there exists a non-zero vector such that the matrix transformation scales the vector without changing its direction. Solving the characteristic polynomial by setting it to zero yields all eigenvalues, providing critical insights into the properties of the matrix.

Characteristic polynomial Infographic