Market risk refers to the potential financial loss you may experience due to fluctuations in market prices, including changes in stocks, bonds, commodities, and currencies. This type of risk is inherent in investing and can be influenced by economic events, political instability, and changes in interest rates. Explore the full article to better understand how to manage market risk effectively and protect your investments.

Table of Comparison

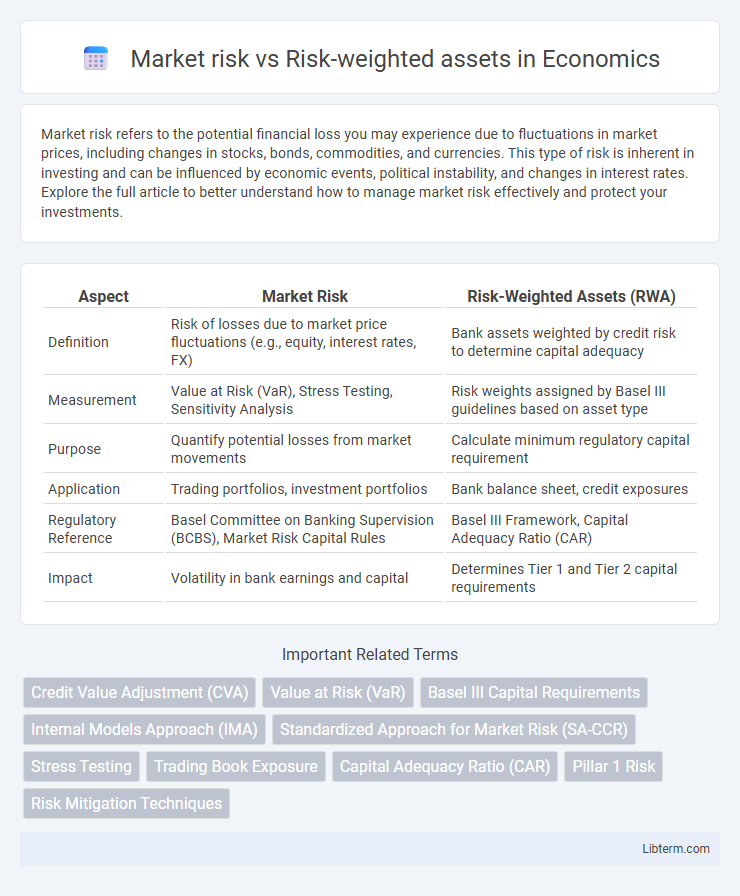

| Aspect | Market Risk | Risk-Weighted Assets (RWA) |

|---|---|---|

| Definition | Risk of losses due to market price fluctuations (e.g., equity, interest rates, FX) | Bank assets weighted by credit risk to determine capital adequacy |

| Measurement | Value at Risk (VaR), Stress Testing, Sensitivity Analysis | Risk weights assigned by Basel III guidelines based on asset type |

| Purpose | Quantify potential losses from market movements | Calculate minimum regulatory capital requirement |

| Application | Trading portfolios, investment portfolios | Bank balance sheet, credit exposures |

| Regulatory Reference | Basel Committee on Banking Supervision (BCBS), Market Risk Capital Rules | Basel III Framework, Capital Adequacy Ratio (CAR) |

| Impact | Volatility in bank earnings and capital | Determines Tier 1 and Tier 2 capital requirements |

Introduction to Market Risk and Risk-Weighted Assets

Market risk refers to the potential financial loss arising from fluctuations in market prices such as interest rates, equity prices, and foreign exchange rates. Risk-weighted assets (RWAs) are a bank's assets weighted by credit risk according to standardized regulatory formulas to determine the minimum capital requirement. Understanding market risk and RWAs is critical for financial institutions to measure exposure and maintain adequate capital buffers under regulatory frameworks like Basel III.

Defining Market Risk

Market risk refers to the potential for financial losses due to fluctuations in market prices, interest rates, foreign exchange rates, or commodity prices. Risk-weighted assets (RWA) measure the total exposure of a financial institution, adjusted by risk factors assigned to different asset classes, including market risk components. Understanding market risk is essential for calculating RWAs, as it impacts the capital requirements banks must hold to absorb potential losses from market volatility.

Understanding Risk-Weighted Assets (RWA)

Risk-weighted assets (RWA) represent a bank's assets adjusted for credit, market, and operational risks to determine regulatory capital requirements. Market risk reflects potential losses due to fluctuations in market variables such as interest rates, exchange rates, and equity prices, directly influencing the RWA calculation under Basel III regulations. Accurate understanding of RWA enables financial institutions to allocate capital efficiently, manage risk exposure, and comply with international regulatory standards.

Key Differences Between Market Risk and RWA

Market risk measures potential losses from fluctuations in market prices, including equity, interest rate, and currency risks, while Risk-Weighted Assets (RWA) quantify the total assets weighted by credit risk to determine capital requirements under regulatory frameworks like Basel III. Market risk is primarily concerned with external market factors affecting asset values, whereas RWA focuses on the internal risk profile of a bank's asset portfolio for regulatory capital adequacy. Understanding these differences is crucial for effective risk management, capital allocation, and compliance with financial regulations.

How Market Risk Impacts Financial Institutions

Market risk significantly affects financial institutions by exposing them to losses from fluctuations in interest rates, foreign exchange rates, and equity prices, which can erode capital and reduce profitability. Risk-weighted assets (RWAs) quantify the level of market risk by assigning different risk weights to various asset classes, directly influencing a bank's capital requirements under regulatory frameworks like Basel III. Effective management of market risk through stress testing and value-at-risk models is essential for maintaining capital adequacy and ensuring long-term financial stability.

The Role of RWA in Regulatory Compliance

Risk-weighted assets (RWA) play a critical role in regulatory compliance by quantifying the credit, market, and operational risks a financial institution faces, allowing regulators to assess capital adequacy effectively. Market risk influences RWA calculations by requiring banks to hold sufficient capital reserves against potential losses from fluctuating asset prices. Regulatory frameworks like Basel III mandate specific capital ratios based on RWA to ensure banks maintain financial stability and absorb market shocks.

Calculating Market Risk: Methods and Metrics

Calculating market risk involves quantifying potential losses due to fluctuations in market prices using metrics such as Value at Risk (VaR), Expected Shortfall (ES), and stress testing. These methods assess the impact of adverse movements in interest rates, equity prices, foreign exchange, and commodity prices on a financial institution's portfolio. Risk-weighted assets (RWA) then incorporate market risk into regulatory capital requirements by assigning risk weights based on the calculated market risk exposure to determine the capital banks must hold to cover potential losses.

Determining Risk-Weighted Assets: Approaches and Frameworks

Determining risk-weighted assets involves quantifying market risk exposure within a bank's trading and investment portfolios using standardized or internal models approaches. The standardized approach allocates risk weights based on predefined regulatory formulas, while the Internal Models Approach (IMA) employs Value-at-Risk (VaR) and stressed VaR models to capture market volatility and tail risks more accurately. Regulatory frameworks such as Basel III mandate these approaches, ensuring banks maintain adequate capital buffers aligned with the market risk embedded in their risk-weighted assets for enhanced financial stability.

Market Risk vs RWA: Implications for Capital Adequacy

Market risk represents the potential loss due to fluctuations in market prices, while risk-weighted assets (RWA) quantify a bank's assets adjusted for their risk levels, directly impacting capital requirements. Higher market risk increases the capital banks must hold under regulatory frameworks like Basel III, influencing the calculation of RWA and capital adequacy ratios. Effective management of market risk reduces RWA volatility, ensuring banks maintain sufficient capital buffers to absorb potential losses and sustain financial stability.

Conclusion: Managing Market Risk and RWA Effectively

Effective management of market risk and risk-weighted assets (RWA) is crucial for maintaining financial stability and regulatory compliance in banking institutions. By employing advanced risk assessment models and stress testing, firms can optimize capital allocation and minimize unexpected losses. Integrating market risk insights with RWA calculations enhances decision-making and supports sustainable growth.

Market risk Infographic