A probability measure quantifies the likelihood of events within a defined sample space, assigning values between 0 and 1 to represent impossibility and certainty, respectively. It adheres to axioms such as non-negativity, normalization, and countable additivity, ensuring consistency and mathematical rigor in probabilistic analysis. Explore the rest of the article to deepen your understanding of how probability measures underpin statistical modeling and decision-making.

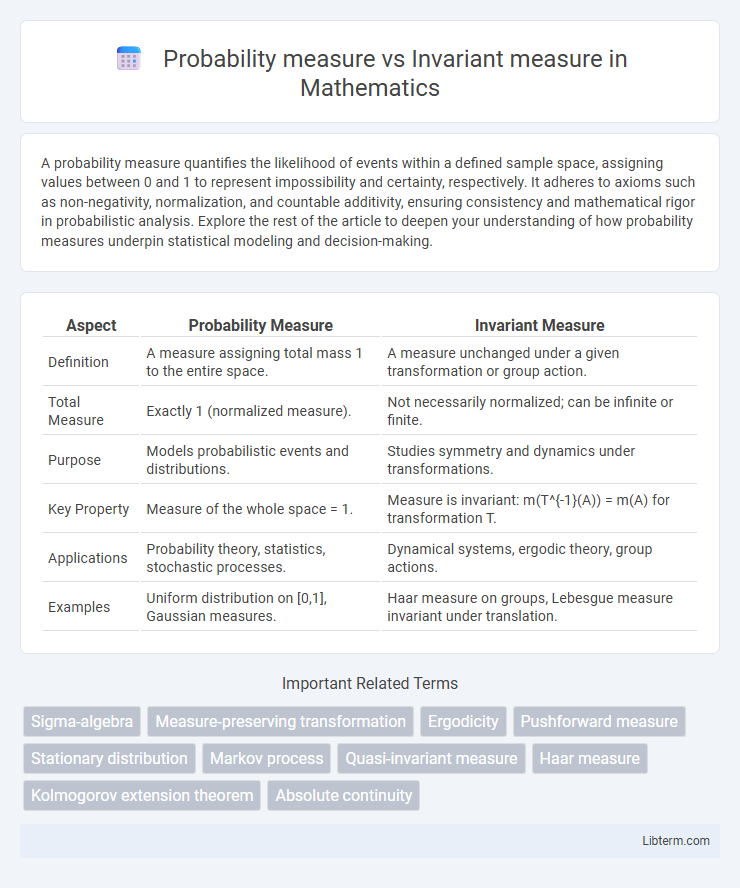

Table of Comparison

| Aspect | Probability Measure | Invariant Measure |

|---|---|---|

| Definition | A measure assigning total mass 1 to the entire space. | A measure unchanged under a given transformation or group action. |

| Total Measure | Exactly 1 (normalized measure). | Not necessarily normalized; can be infinite or finite. |

| Purpose | Models probabilistic events and distributions. | Studies symmetry and dynamics under transformations. |

| Key Property | Measure of the whole space = 1. | Measure is invariant: m(T^{-1}(A)) = m(A) for transformation T. |

| Applications | Probability theory, statistics, stochastic processes. | Dynamical systems, ergodic theory, group actions. |

| Examples | Uniform distribution on [0,1], Gaussian measures. | Haar measure on groups, Lebesgue measure invariant under translation. |

Introduction to Probability Measure and Invariant Measure

A probability measure assigns a non-negative value to events in a sigma-algebra, ensuring the total measure of the entire space equals one, which forms the foundation of probability theory. An invariant measure remains unchanged under the action of a transformation or dynamical system, playing a crucial role in ergodic theory and statistical mechanics. Both concepts use measure theory but serve distinct purposes: probability measures quantify uncertainty, while invariant measures describe steady-state distributions under dynamics.

Fundamental Concepts of Measure Theory

Probability measures assign values between 0 and 1 to events within a sigma-algebra, ensuring the total measure of the entire space is 1, reflecting the likelihood of outcomes. Invariant measures maintain their measure under transformations or group actions, preserving the structure of the space and playing a crucial role in ergodic theory and dynamical systems. Both concepts rely on sigma-algebras and measurable spaces, fundamental constructs in measure theory that formalize the assignment of measures to sets and support integration and convergence theorems.

What is a Probability Measure?

A probability measure is a function that assigns a value between 0 and 1 to subsets of a given sample space, representing the likelihood of events within that space, with the total measure of the entire space equal to 1. It satisfies the axioms of non-negativity, normalization, and countable additivity, ensuring consistent probability assignments for events. In contrast, an invariant measure remains unchanged under the dynamics of a system, often used in ergodic theory to describe long-term statistical behavior rather than direct event likelihoods.

Understanding Invariant Measure

Invariant measure is a type of probability measure that remains unchanged under the dynamics of a given system, making it fundamental in ergodic theory and statistical mechanics. It provides a stable description of the long-term behavior of a system by satisfying the condition m(T-1(A)) = m(A) for measurable sets A under the transformation T. Unlike general probability measures, invariant measures capture equilibrium distributions essential for analyzing steady states and recurrence properties in dynamical systems.

Key Differences: Probability Measure vs Invariant Measure

A probability measure assigns a non-negative value to events in a sigma-algebra, summing to one, reflecting the likelihood of outcomes in a probabilistic space. An invariant measure, often used in dynamical systems, remains unchanged under the system's transformations, preserving measure across iterations or flows. The key difference lies in their purpose: probability measures quantify randomness, while invariant measures describe steady-state distributions or conserved quantities under specific mappings.

Mathematical Properties and Definitions

A probability measure is a function defined on a sigma-algebra that assigns a value between 0 and 1 to each measurable set, satisfying countable additivity and normalization to 1, ensuring a total measure of one over the entire space. An invariant measure remains unchanged under the action of a measurable transformation or a dynamical system, meaning the measure of any measurable set equals the measure of its preimage under the transformation. The core mathematical distinction lies in probability measures emphasizing total mass normalization, while invariant measures focus on preserving measure under transformations, often applied in ergodic theory and dynamical systems.

Common Applications in Mathematics and Physics

Probability measures quantify the likelihood of events in stochastic processes and are fundamental in fields like statistical mechanics and ergodic theory. Invariant measures remain constant under transformations, playing a crucial role in dynamical systems, chaos theory, and Hamiltonian mechanics to describe equilibrium states. Both measures underpin the analysis of long-term system behavior, with probability measures emphasizing randomness and invariant measures highlighting structural stability.

Examples Illustrating Both Measures

A probability measure assigns a total measure of one to the entire sample space, commonly illustrated by the probability of outcomes in a fair die roll where each face has a measure of one-sixth. An invariant measure remains unchanged under the dynamics of a system, such as the Lebesgue measure on the unit interval [0,1] under a rotation map modulo 1. While the probability measure quantifies likelihoods in stochastic processes, the invariant measure captures long-term steady-state distributions in dynamical systems, exemplified by the uniform distribution on a circle remaining stable under angular rotations.

Importance in Ergodic Theory and Dynamics

Probability measures provide a foundational framework for quantifying uncertainty in dynamical systems, assigning total mass one to the space which ensures meaningful probabilistic interpretation. Invariant measures remain unchanged under the dynamics, capturing the long-term statistical behavior and enabling the study of ergodic properties. Their interplay is crucial in ergodic theory, as invariant probability measures allow decomposition of systems into ergodic components, facilitating analysis of stability, recurrence, and equilibrium states.

Summary and Further Reading

Probability measures quantify the likelihood of events within a measurable space, assigning values between 0 and 1 that sum to 1, while invariant measures remain unchanged under a given transformation, often used to study dynamical systems and ergodic theory. The distinction lies in functionality: probability measures evaluate randomness, whereas invariant measures analyze the stability and long-term behavior of transformations. For further reading, explore texts on measure theory, ergodic theory, and dynamical systems, such as "Ergodic Theory" by Karl Petersen and "Measure Theory" by Paul Halmos.

Probability measure Infographic