A linear production function defines output as a constant proportion of input, expressed mathematically as Q = aL + b, where Q is output, L is labor input, and a and b are constants. This function assumes no diminishing returns, meaning each additional unit of input increases output by the same amount. Discover how understanding this function can improve your efficiency by reading the rest of the article.

Table of Comparison

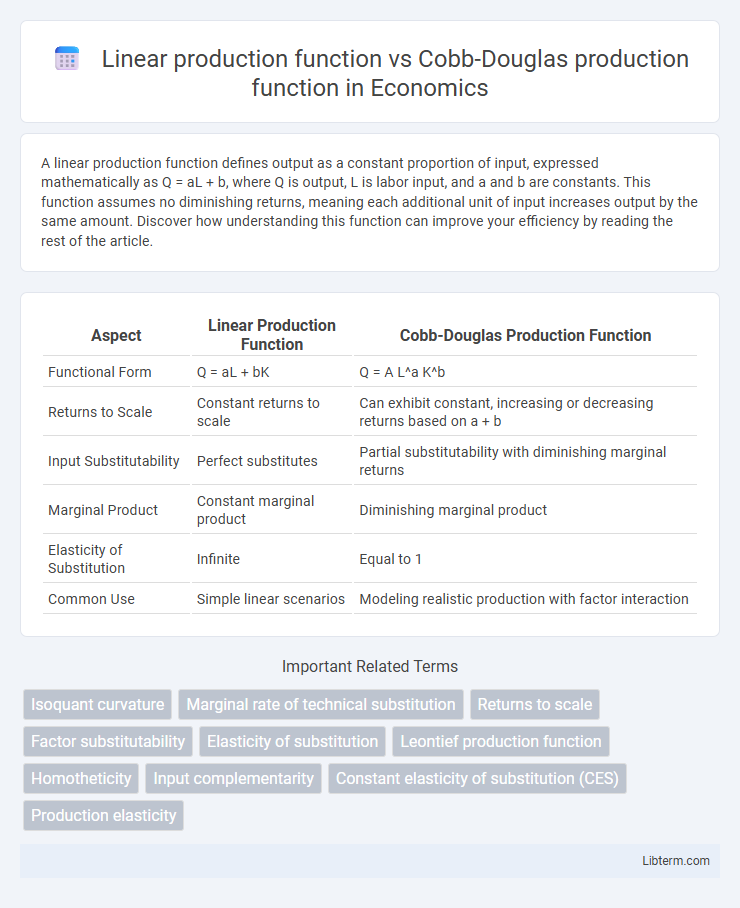

| Aspect | Linear Production Function | Cobb-Douglas Production Function |

|---|---|---|

| Functional Form | Q = aL + bK | Q = A L^a K^b |

| Returns to Scale | Constant returns to scale | Can exhibit constant, increasing or decreasing returns based on a + b |

| Input Substitutability | Perfect substitutes | Partial substitutability with diminishing marginal returns |

| Marginal Product | Constant marginal product | Diminishing marginal product |

| Elasticity of Substitution | Infinite | Equal to 1 |

| Common Use | Simple linear scenarios | Modeling realistic production with factor interaction |

Introduction to Production Functions

The Linear production function assumes constant returns to scale with fixed input proportions, expressed as Q = aL + bK, where output increases linearly with labor (L) and capital (K). In contrast, the Cobb-Douglas production function, given by Q = A L^a K^b, features variable returns to scale and allows for substitution between inputs, capturing diminishing marginal returns through exponents a and b. These production functions serve as foundational tools in economics to model the relationship between input factors and output, facilitating analysis of efficiency and productivity.

Overview of Linear Production Function

The linear production function represents output as a straightforward sum of inputs multiplied by constant coefficients, indicating constant marginal productivity and perfect substitutability between inputs. It assumes that increasing one input while holding others fixed results in a proportional increase in output, making it simpler but less realistic than nonlinear models. This function contrasts with the Cobb-Douglas production function, which captures diminishing marginal returns and input interactions through multiplicative terms with exponents representing input elasticities.

Key Features of Cobb-Douglas Production Function

The Cobb-Douglas production function is characterized by its multiplicative form involving inputs raised to constant elasticities, reflecting diminishing marginal returns and exhibiting constant returns to scale when exponents sum to one. It incorporates factor substitutability through continuous partial derivatives, allowing more realistic modeling of input interactions compared to the linear production function's fixed input-output relationship. The function's flexibility in parameterizing the output elasticity of labor and capital makes it widely used in empirical economic analyses and growth models.

Mathematical Formulation: Linear vs Cobb-Douglas

The Linear production function is mathematically represented as Q = aL + bK, where Q is output, L is labor, K is capital, and a, b are constants indicating marginal products. In contrast, the Cobb-Douglas production function is expressed as Q = A L^a K^b, with A as total factor productivity, and a, b as output elasticities of labor and capital, reflecting diminishing marginal returns. The Linear function assumes constant marginal productivity, while Cobb-Douglas captures variable returns to scale through its multiplicative and exponential form.

Assumptions Underlying Each Model

The linear production function assumes constant marginal returns to each input, implying perfect substitutability between labor and capital with fixed coefficients, while the Cobb-Douglas production function assumes diminishing marginal returns and a specific elasticity of substitution between inputs. The linear model posits constant returns to scale with additive separability, whereas the Cobb-Douglas model ensures constant returns to scale but allows for multiplicative interaction of inputs reflecting more realistic input complementarities. Both models rely on smooth and continuous production processes, but the Cobb-Douglas function incorporates flexibility in factor shares and responsiveness to input changes, unlike the rigid fixed proportions in the linear function.

Returns to Scale: Linear vs Cobb-Douglas

Linear production functions exhibit constant returns to scale, meaning output increases proportionally with input increments, reflecting a straightforward additive relationship between inputs and output. In contrast, Cobb-Douglas production functions allow for variable returns to scale, characterized by the sum of output elasticities of inputs: if the sum equals one, returns to scale are constant; greater than one indicates increasing returns to scale; less than one denotes decreasing returns to scale. This flexibility in the Cobb-Douglas model enables more precise modeling of real-world production processes compared to the rigid linear function.

Elasticity of Substitution Comparison

The elasticity of substitution in a linear production function is infinite, indicating perfect substitutability between inputs, allowing firms to replace one input with another without affecting output. In contrast, the Cobb-Douglas production function has a constant elasticity of substitution equal to one, reflecting a balanced trade-off between inputs where proportional changes in input ratios result in proportional changes in the marginal rate of technical substitution. This distinction critically impacts input combination flexibility and production responsiveness to input price changes in economic modeling.

Applicability in Real-World Scenarios

The Linear production function, characterized by constant marginal returns to each input, is best suited for scenarios with fixed input proportions and simple scaling, making it ideal for short-term or small-scale operations. In contrast, the Cobb-Douglas production function captures variable elasticities of substitution between inputs, accommodating diminishing marginal returns and scalability, which aligns better with complex industries like manufacturing, agriculture, and technology sectors. Empirical studies show Cobb-Douglas models provide more accurate representations of output variations in economies where input flexibility and technological progress play significant roles.

Advantages and Limitations of Each Function

The Linear production function offers simplicity and ease of interpretation, making it useful for modeling fixed input-output relationships but lacks flexibility in capturing diminishing returns or input substitution, limiting its realism in complex production scenarios. The Cobb-Douglas production function provides a more flexible framework by allowing variable returns to scale and input substitutability, effectively modeling diminishing marginal productivity, yet its assumption of constant elasticity of substitution and specific functional form may oversimplify actual production processes. Both functions serve distinct purposes: Linear models are advantageous for straightforward, proportional input-output analysis, while Cobb-Douglas models excel in representing nuanced economic behaviors and input interactions.

Conclusion: Choosing the Right Production Function

The choice between a linear production function and a Cobb-Douglas production function depends on the nature of returns to scale and input substitutability in the production process. Linear production functions assume constant marginal returns and perfect substitutability between inputs, ideal for simplistic or proportional growth scenarios, while Cobb-Douglas functions capture variable returns to scale and diminishing marginal productivity, reflecting more realistic input interactions. Businesses and economists select the appropriate model based on empirical data, production complexity, and the need for flexibility in analyzing input-output relationships.

Linear production function Infographic