Stationary objects remain fixed in one position, unaffected by external forces or motion. Understanding the concept of stationary is essential in fields like physics, engineering, and design, as it impacts stability and structure. Explore the rest of the article to learn how stationary elements influence various applications and your daily life.

Table of Comparison

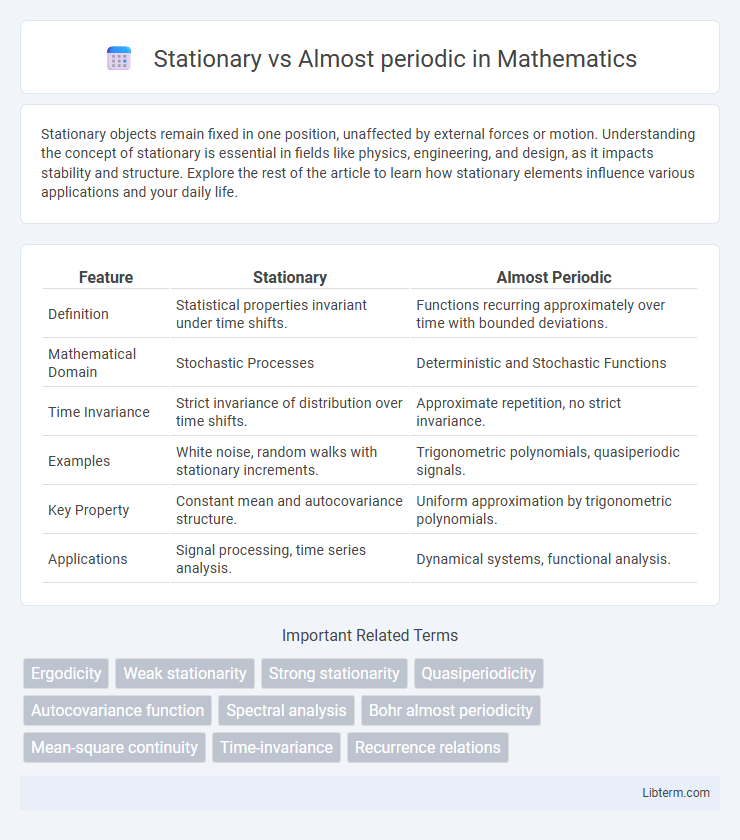

| Feature | Stationary | Almost Periodic |

|---|---|---|

| Definition | Statistical properties invariant under time shifts. | Functions recurring approximately over time with bounded deviations. |

| Mathematical Domain | Stochastic Processes | Deterministic and Stochastic Functions |

| Time Invariance | Strict invariance of distribution over time shifts. | Approximate repetition, no strict invariance. |

| Examples | White noise, random walks with stationary increments. | Trigonometric polynomials, quasiperiodic signals. |

| Key Property | Constant mean and autocovariance structure. | Uniform approximation by trigonometric polynomials. |

| Applications | Signal processing, time series analysis. | Dynamical systems, functional analysis. |

Understanding Stationary Processes

Stationary processes maintain consistent statistical properties, such as mean and autocorrelation, over time, making them essential in time series analysis for modeling stable phenomena. Almost periodic processes exhibit recurring patterns with frequencies that are not strictly periodic but still repeat in a generalized sense, useful in capturing signals with quasi-periodic behavior. Understanding stationary processes involves recognizing their invariance under time shifts, which underpins tools like spectral density estimation and forecasting in econometrics and engineering.

Defining Almost Periodic Functions

Almost periodic functions generalize stationary functions by exhibiting recurrent patterns that approximate periodicity without a fixed period. Unlike strictly periodic functions with an exact period, almost periodic functions maintain uniform approximation by trigonometric polynomials over the entire real line. This concept plays a crucial role in harmonic analysis and applications where signals or systems display stability without strict periodic repetition.

Key Differences Between Stationary and Almost Periodic

Stationary processes have statistical properties that remain constant over time, making their mean, variance, and autocorrelation independent of time shifts. Almost periodic processes exhibit recurring patterns with frequencies that are not strictly periodic but uniformly approximate periodic components, allowing their behavior to be described by a finite sum of exponentials. The key difference lies in stationarity involving time-invariant statistics, while almost periodicity involves predictably recurring, but not strictly periodic, structural patterns.

Mathematical Foundations

Stationary processes exhibit statistical properties invariant under time shifts, characterized by constant mean and autocovariance functions dependent only on time differences. Almost periodic functions, defined by Bohr's theory, generalize periodicity with uniform approximation by trigonometric polynomials, capturing recurrent yet non-strictly periodic behavior. The mathematical foundation connects stationary processes to spectral measures via the Wiener-Khinchin theorem, while almost periodicity involves Fourier series expansions with frequencies forming a relatively dense set, enabling analysis beyond strict stationarity.

Applications in Time Series Analysis

Stationary time series exhibit constant statistical properties over time, making them ideal for modeling and forecasting in econometrics and signal processing. Almost periodic time series extend this concept by allowing recurring patterns with varying amplitude and frequency, improving analysis in climatology and biomedical signal detection. Utilizing almost periodic models captures complex cyclic behaviors otherwise missed by strict stationarity assumptions, enhancing prediction accuracy and anomaly detection.

Examples in Signal Processing

Stationary signals maintain statistical properties such as mean and autocorrelation constant over time, exemplified by white noise and Gaussian noise in signal processing applications. Almost periodic signals, like chirp signals and certain types of modulated waves, exhibit quasi-repetitive patterns without strict periodicity, allowing for more complex frequency analysis using tools like Fourier or wavelet transforms. Understanding these differences aids in designing filters and detectors tailored for stochastic processes versus deterministic but irregular signals.

Advantages and Limitations

Stationary processes provide consistent statistical properties over time, making them ideal for modeling stable systems and simplifying analysis through techniques like spectral density estimation. Almost periodic functions capture evolving but recurrent patterns, offering flexibility in modeling signals with quasi-periodic behavior found in fields such as climatology and economics. However, stationary models may fail to represent non-stationary trends, while almost periodic functions can be more complex to estimate and interpret due to their less strict regularity.

Detection and Analysis Techniques

Detection and analysis techniques for stationary and almost periodic signals differ significantly due to their distinct statistical properties; stationary signals exhibit constant mean and variance over time, making techniques like autocorrelation and power spectral density effective for identifying consistent frequency components. Almost periodic signals, characterized by frequencies that recur with bounded but non-constant intervals, require advanced methods such as Fourier series expansions and time-frequency analysis tools like wavelet transforms to capture their quasi-periodic patterns. Effective detection hinges on distinguishing stable statistical features in stationary signals from the more complex, slowly varying frequency structures inherent in almost periodic signals.

Real-World Use Cases

Stationary processes are widely used in econometrics for modeling time series data with constant mean and variance, such as stock prices or climate data analysis, enabling reliable forecasting and risk assessment. Almost periodic processes capture signals with recurrent but non-strictly periodic patterns, essential for modeling biological rhythms or communication signals with quasi-periodic fluctuations. Real-world applications leverage stationary assumptions for stability in financial models, while almost periodic frameworks enhance detection of complex cyclic behaviors in engineering and neuroscience.

Summary and Future Perspectives

Stationary processes exhibit statistical properties invariant over time, while almost periodic processes display recurring patterns with potentially evolving frequencies and amplitudes. Future research aims to deepen the mathematical characterization of almost periodicity in stochastic models and enhance signal processing techniques for complex datasets. Integrating machine learning approaches may improve prediction accuracy and broaden applications in engineering and finance.

Stationary Infographic