Cash accounting records transactions only when cash changes hands, providing a straightforward way to track income and expenses. This method is often favored by small businesses and individuals for its simplicity and clear cash flow visibility. Explore the full article to understand how cash accounting can benefit your financial management.

Table of Comparison

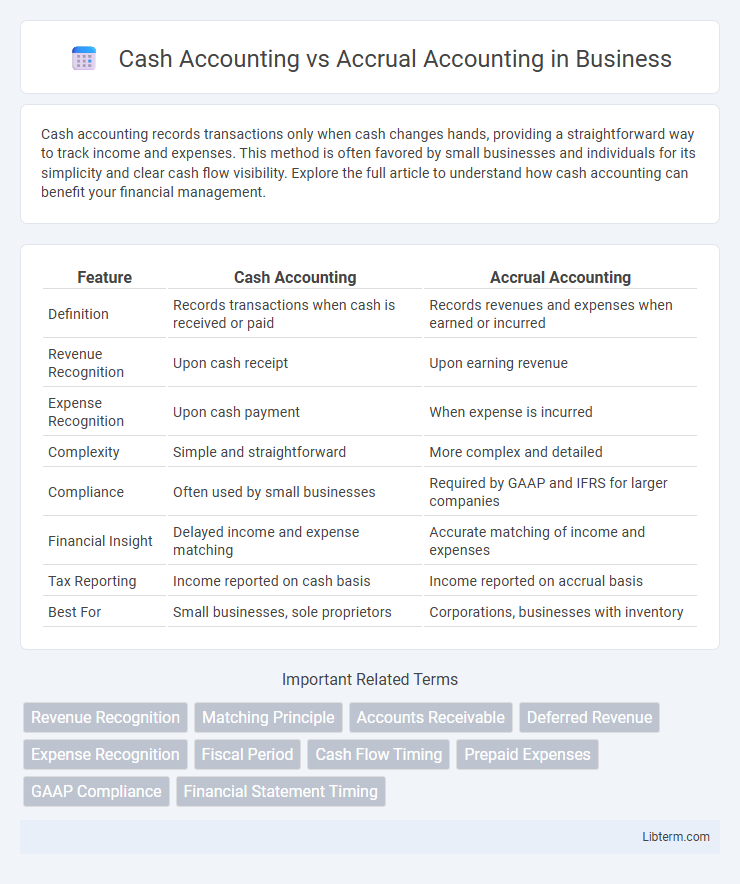

| Feature | Cash Accounting | Accrual Accounting |

|---|---|---|

| Definition | Records transactions when cash is received or paid | Records revenues and expenses when earned or incurred |

| Revenue Recognition | Upon cash receipt | Upon earning revenue |

| Expense Recognition | Upon cash payment | When expense is incurred |

| Complexity | Simple and straightforward | More complex and detailed |

| Compliance | Often used by small businesses | Required by GAAP and IFRS for larger companies |

| Financial Insight | Delayed income and expense matching | Accurate matching of income and expenses |

| Tax Reporting | Income reported on cash basis | Income reported on accrual basis |

| Best For | Small businesses, sole proprietors | Corporations, businesses with inventory |

Introduction to Cash and Accrual Accounting

Cash accounting records financial transactions only when cash changes hands, providing a straightforward view of cash flow suitable for small businesses. Accrual accounting recognizes income and expenses when they are earned or incurred, offering a more accurate financial picture by matching revenues with related costs. Understanding the difference between cash and accrual accounting is essential for selecting the appropriate method that aligns with business size, complexity, and tax requirements.

Key Differences Between Cash and Accrual Methods

Cash accounting records transactions only when cash changes hands, providing a straightforward view of actual cash flow, while accrual accounting recognizes income and expenses when they are earned or incurred, regardless of payment timing. This difference significantly impacts financial statements, with accrual accounting offering a more accurate picture of long-term financial health by matching revenues with related expenses. Businesses with complex operations or inventory typically prefer accrual accounting for its comprehensive tracking of economic activities.

How Cash Accounting Works

Cash accounting records revenues and expenses only when cash is actually received or paid, providing a clear snapshot of cash flow. Transactions are recognized at the time of physical cash exchange, making it simpler for small businesses to track liquidity. This method avoids accounts receivable and payable, emphasizing immediate financial impact rather than future obligations.

How Accrual Accounting Works

Accrual accounting records revenues and expenses when they are earned or incurred, regardless of cash flow timing, providing a more accurate financial picture. This method matches income with related expenses within the same period, enhancing financial analysis and decision-making. Businesses using accrual accounting comply with GAAP standards and gain better insights into long-term profitability and financial health.

Pros and Cons of Cash Accounting

Cash accounting offers simplicity and immediate clarity by recording transactions only when cash changes hands, making it ideal for small businesses and individuals with straightforward finances. This method provides real-time cash flow visibility but can misrepresent financial health by ignoring outstanding liabilities and receivables. However, cash accounting may limit financial analysis and tax planning opportunities compared to accrual accounting, which records income and expenses when incurred.

Pros and Cons of Accrual Accounting

Accrual accounting offers a comprehensive view of a company's financial health by recording revenues and expenses when they are earned or incurred, providing more accurate insights for long-term decision-making. However, it can be complex to implement and manage, requiring detailed tracking of accounts receivable and payable, which may demand more advanced accounting systems and expertise. This method may also present a misleading picture of immediate cash flow, as profits shown on financial statements do not necessarily reflect actual cash available.

Suitability for Different Business Types

Cash accounting suits small businesses and sole proprietors with straightforward transactions, allowing them to record income and expenses only when money changes hands. Accrual accounting is preferable for larger businesses and those with inventory or credit sales, as it records revenues and expenses when they are incurred, providing a more accurate financial picture. Companies aiming for compliance with GAAP or seeking investors often adopt accrual accounting due to its comprehensive financial reporting.

Impact on Financial Reporting and Taxes

Cash accounting records transactions only when cash changes hands, resulting in simpler financial statements with income and expenses recognized immediately, which can reduce taxable income in the short term by deferring revenue recognition. Accrual accounting matches revenues and expenses to the period they relate to, providing a more accurate financial picture and better compliance with Generally Accepted Accounting Principles (GAAP), but may increase taxable income by recognizing revenue before cash receipt. The choice between cash and accrual accounting directly impacts the timing of tax liabilities and financial reporting accuracy, influencing decision-making for businesses and tax authorities.

Transitioning Between Cash and Accrual Accounting

Transitioning between cash and accrual accounting requires careful adjustment of revenue and expense recognition to align with the chosen method's principles. Businesses must reconcile outstanding receivables, payables, and inventory values to accurately reflect financial position under accrual accounting. Implementing accounting software that supports both methods can streamline the transition and ensure compliance with Generally Accepted Accounting Principles (GAAP).

Choosing the Right Method for Your Business

Cash accounting recognizes revenue and expenses only when money changes hands, making it ideal for small businesses with simple transactions and a focus on cash flow management. Accrual accounting records income and expenses when they are earned or incurred, providing a more accurate financial picture for businesses with inventory, credit sales, or complex operations. Selecting the right accounting method depends on business size, regulatory requirements, and the need for detailed financial reporting to support decision-making and growth.

Cash Accounting Infographic