Gamma rays are a form of electromagnetic radiation with extremely high energy and short wavelengths, capable of penetrating most materials. These rays are commonly produced by nuclear reactions, cosmic events, and certain radioactive substances, making them crucial in medical imaging and cancer treatment. Discover how gamma rays impact technology and health in the rest of the article.

Table of Comparison

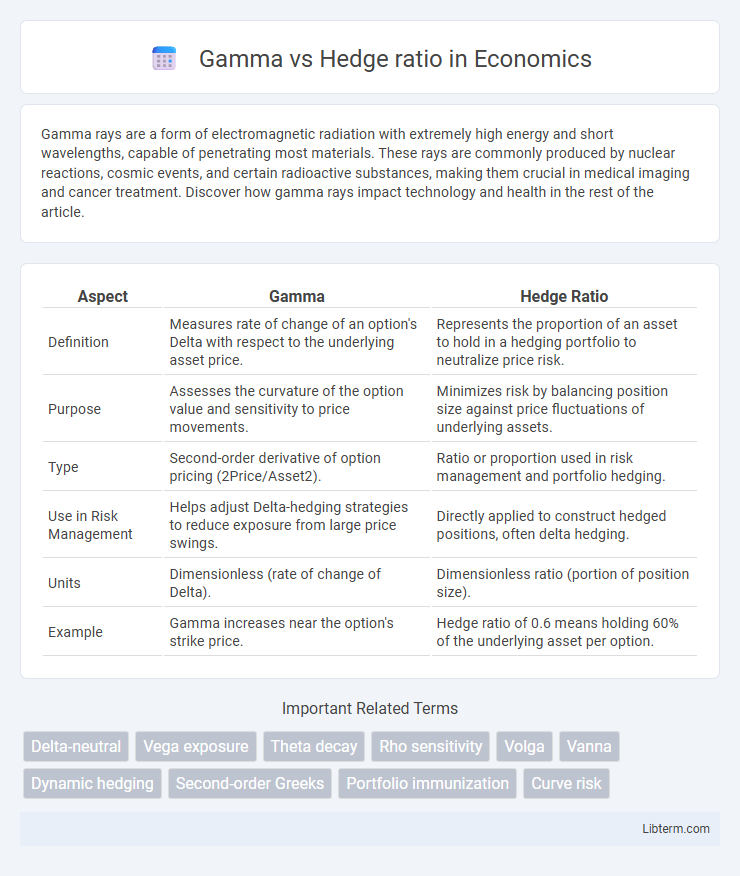

| Aspect | Gamma | Hedge Ratio |

|---|---|---|

| Definition | Measures rate of change of an option's Delta with respect to the underlying asset price. | Represents the proportion of an asset to hold in a hedging portfolio to neutralize price risk. |

| Purpose | Assesses the curvature of the option value and sensitivity to price movements. | Minimizes risk by balancing position size against price fluctuations of underlying assets. |

| Type | Second-order derivative of option pricing (2Price/Asset2). | Ratio or proportion used in risk management and portfolio hedging. |

| Use in Risk Management | Helps adjust Delta-hedging strategies to reduce exposure from large price swings. | Directly applied to construct hedged positions, often delta hedging. |

| Units | Dimensionless (rate of change of Delta). | Dimensionless ratio (portion of position size). |

| Example | Gamma increases near the option's strike price. | Hedge ratio of 0.6 means holding 60% of the underlying asset per option. |

Understanding Gamma and Hedge Ratio: Key Concepts

Gamma measures the rate of change of an option's delta with respect to the underlying asset price, providing insight into the option's sensitivity to price movements. The hedge ratio, commonly represented by delta, indicates the proportion of the underlying asset needed to hedge against price risk, optimizing portfolio protection. Understanding the interplay between gamma and hedge ratio is crucial for dynamic risk management and adjusting hedging positions as market conditions evolve.

The Role of Gamma in Options Trading

Gamma measures the rate of change of an option's delta relative to the underlying asset's price, playing a crucial role in managing an options portfolio's sensitivity to price movements. Traders use gamma to understand how delta will shift as the underlying asset price changes, which is essential for dynamic hedging strategies. High gamma values indicate more significant adjustments to delta, helping traders mitigate risks by maintaining an effective hedge ratio.

Hedge Ratio Explained: Definition and Importance

The hedge ratio measures the proportion of an asset's exposure offset by a derivative or hedge to minimize risk, commonly used in options trading and portfolio management. It quantifies how much of the underlying asset is needed to hedge against price movements, making it essential for managing volatility and protecting investments. Understanding the hedge ratio enables traders to implement effective risk management strategies by aligning the hedged position with market movements.

Gamma vs Hedge Ratio: Core Differences

Gamma measures the rate of change of an option's delta relative to price movements in the underlying asset, reflecting the curvature of the option's value. The hedge ratio, often synonymous with delta, represents the proportion of the underlying asset needed to hedge an options position to remain delta-neutral. While gamma quantifies the sensitivity of delta and informs dynamic hedging adjustments, the hedge ratio provides the baseline ratio for initial hedging decisions in options trading.

Calculating Gamma and Hedge Ratio in Practice

Calculating Gamma involves determining the second derivative of an option's price relative to the underlying asset's price, quantifying the rate of change of Delta, which is essential for managing the convexity of option positions. The Hedge Ratio, commonly represented by Delta, indicates the proportion of the underlying asset needed to maintain a delta-neutral position, calculated as the first derivative of the option price with respect to the underlying price. In practice, traders use numerical methods or option pricing models like Black-Scholes to estimate Gamma and Hedge Ratio, adjusting their portfolios dynamically to mitigate risk from price movements.

Impact of Volatility on Gamma and Hedge Ratio

Gamma measures the rate of change in an option's delta relative to price movements of the underlying asset, significantly impacting hedging strategies during periods of high volatility. Increased volatility typically causes Gamma to spike, making the hedge ratio more sensitive and requiring frequent adjustments to maintain a delta-neutral position. Understanding the dynamic relationship between volatility, Gamma, and the hedge ratio is essential for effective risk management in options trading.

Managing Risk: Gamma Hedging Strategies

Gamma hedging strategies enhance risk management by stabilizing a portfolio's delta exposure through the adjustment of underlying assets or options, thereby mitigating the impact of rapid price movements. By maintaining a neutral gamma position, traders limit the sensitivity of delta to price changes, reducing potential losses from volatility spikes. Implementing dynamic gamma hedging requires continuous monitoring and rebalancing, making it essential for managing the convexity risks inherent in options portfolios.

Practical Applications: When to Use Gamma or Hedge Ratio

Gamma measures the rate of change in an option's delta, making it crucial for managing portfolios with significant directional risk or rapid market movements. Hedge ratio, or delta, indicates the number of shares needed to hedge an option position's price risk, ideal for maintaining a neutral portfolio in stable or slower-moving markets. Traders use gamma to adjust hedges dynamically during high volatility, while hedge ratio provides a baseline for initial position adjustments.

Gamma and Hedge Ratio in Portfolio Management

Gamma measures the rate of change of an option's delta relative to the underlying asset's price, playing a crucial role in managing portfolio risk by indicating sensitivity to price movements. Hedge ratio, often represented by delta, determines the proportion of the underlying asset needed to hedge against price changes in an option position, ensuring effective risk mitigation. Portfolio managers leverage gamma and hedge ratio to dynamically adjust positions, optimizing hedging strategies and enhancing portfolio stability in volatile markets.

Common Mistakes in Gamma and Hedge Ratio Analysis

Common mistakes in Gamma and Hedge Ratio analysis include ignoring the dynamic changes in Gamma as the underlying asset price moves, leading to inaccurate hedging strategies. Another frequent error is treating the Hedge Ratio as static instead of recalculating it regularly to reflect current market conditions and volatility. Misestimating Gamma can cause significant deviations in risk management, particularly in options portfolios where precise adjustments are critical.

Gamma Infographic