The Law of Demand explains that as the price of a good or service decreases, the quantity demanded generally increases, while higher prices typically lead to lower demand. This fundamental principle helps businesses and consumers understand market behavior and make informed decisions about pricing and purchasing. Explore the rest of the article to understand how the Law of Demand impacts markets and your economic choices.

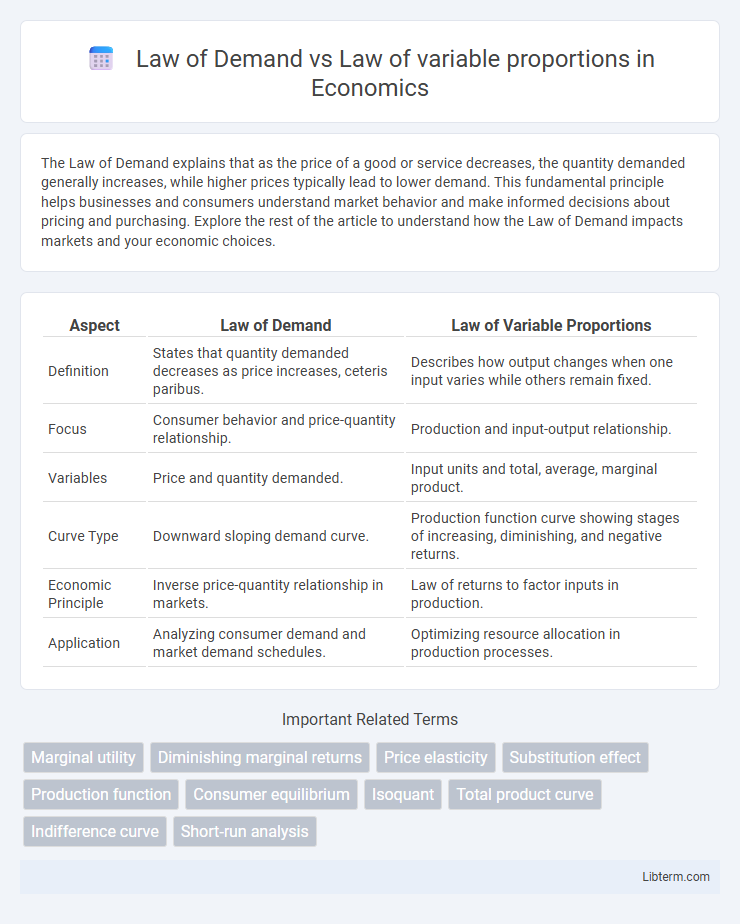

Table of Comparison

| Aspect | Law of Demand | Law of Variable Proportions |

|---|---|---|

| Definition | States that quantity demanded decreases as price increases, ceteris paribus. | Describes how output changes when one input varies while others remain fixed. |

| Focus | Consumer behavior and price-quantity relationship. | Production and input-output relationship. |

| Variables | Price and quantity demanded. | Input units and total, average, marginal product. |

| Curve Type | Downward sloping demand curve. | Production function curve showing stages of increasing, diminishing, and negative returns. |

| Economic Principle | Inverse price-quantity relationship in markets. | Law of returns to factor inputs in production. |

| Application | Analyzing consumer demand and market demand schedules. | Optimizing resource allocation in production processes. |

Introduction to the Law of Demand and Law of Variable Proportions

The Law of Demand states that, ceteris paribus, an increase in the price of a good causes a decrease in its quantity demanded, reflecting an inverse relationship between price and demand. The Law of Variable Proportions explains how output changes when one input factor varies while other inputs remain fixed, illustrating the concept of diminishing marginal returns. Both laws are fundamental to understanding consumer behavior and production efficiency in economics.

Defining the Law of Demand

The Law of Demand states that, ceteris paribus, an increase in the price of a good or service leads to a decrease in the quantity demanded, illustrating an inverse relationship between price and demand. In contrast, the Law of Variable Proportions examines the changes in output when the quantity of one input varies while other inputs remain fixed, emphasizing production rather than consumer behavior. Understanding the Law of Demand is fundamental in microeconomics, as it explains consumer purchasing patterns and market equilibrium.

Key Assumptions of the Law of Demand

The Law of Demand assumes consumer preferences remain constant, meaning buyers will purchase more of a good as its price decreases while other factors stay unchanged (ceteris paribus). It requires a clear substitution effect, where consumers switch to cheaper alternatives, and a diminishing marginal utility, implying the added satisfaction from consuming extra units decreases. These key assumptions ensure the inverse relationship between price and quantity demanded holds true in typical market scenarios.

Defining the Law of Variable Proportions

The Law of Variable Proportions explains how output changes when one input factor is varied while other inputs remain constant, highlighting stages of increasing, constant, and diminishing returns. Unlike the Law of Demand, which describes the inverse relationship between price and quantity demanded, the Law of Variable Proportions focuses on production efficiency and input optimization in the short run. This law is fundamental in understanding how firms adjust input combinations to maximize productivity under fixed resource constraints.

Key Assumptions of the Law of Variable Proportions

The Law of Variable Proportions assumes that technology remains constant and only one input factor varies while others are fixed. It presumes homogenous inputs and outputs, implying uniform quality and consistent production conditions. The time period considered is short enough that factors like capital or technology cannot change, isolating the effect of varying one input on output.

Differences in Scope and Application

The Law of Demand focuses on the inverse relationship between price and quantity demanded for goods and services, primarily applied in consumer behavior analysis and market pricing strategies. In contrast, the Law of Variable Proportions deals with the output changes resulting from varying one input factor while keeping others constant, predominantly used in production and operational efficiency studies. While demand law applies to the consumption side of economics, the variable proportions law targets production processes, reflecting differences in scope and application within economic theory.

Graphical Representation and Explanation

The Law of Demand graphically shows a downward-sloping demand curve, illustrating the inverse relationship between price and quantity demanded, where higher prices lead to lower demand. The Law of Variable Proportions, depicted by the total product curve, demonstrates how output varies with changes in one input while other inputs remain fixed, typically showing increasing, then diminishing returns. In contrast to the demand curve's price-quantity focus, the variable proportions graph emphasizes input-output relationships in production analysis.

Factors Influencing Each Law

The Law of Demand is primarily influenced by factors such as consumer income, preferences, substitute goods availability, and price expectations, which dictate the quantity demanded at various price levels. In contrast, the Law of Variable Proportions depends on factors like the fixed and variable input proportions, technological efficiency, and the stage of production, affecting marginal returns as input quantities change. Both laws reflect core economic principles but operate under distinct conditions shaped by demand-side behavior versus production input dynamics.

Practical Implications in Economics

The Law of Demand highlights the inverse relationship between price and quantity demanded, essential for pricing strategies and consumer behavior analysis in markets. The Law of Variable Proportions explains how output changes with varying input levels, crucial for optimizing production efficiency and resource allocation in firms. Understanding both laws allows economists and businesses to balance cost, output, and pricing for maximizing profit and market competitiveness.

Conclusion: Comparative Summary of Both Laws

The Law of Demand describes the inverse relationship between price and quantity demanded, emphasizing consumer behavior in markets, while the Law of Variable Proportions focuses on the output changes resulting from varying one input factor in production, holding others constant. Demand law primarily addresses market demand elasticity and consumer choices, whereas the variable proportions law explains production efficiency and returns to scale. Both laws are fundamental in understanding economic decision-making, with demand law guiding price-quantity dynamics and variable proportions law illuminating input-output relationships in production processes.

Law of Demand Infographic