Rational expectations theory assumes that individuals use all available information efficiently to forecast future economic variables, leading to predictions that on average are accurate and unbiased. This concept significantly impacts policy analysis, as it suggests that systematic government actions may be anticipated and neutralized by economic agents. Explore how rational expectations influence market behavior and economic policymaking in the rest of this article.

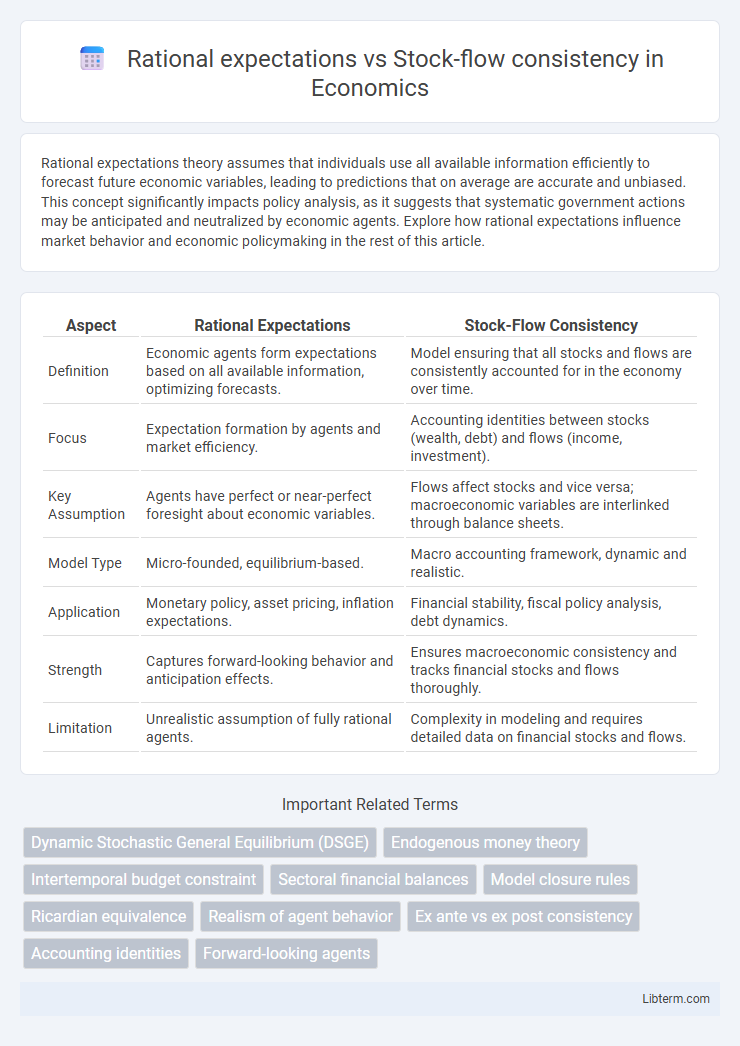

Table of Comparison

| Aspect | Rational Expectations | Stock-Flow Consistency |

|---|---|---|

| Definition | Economic agents form expectations based on all available information, optimizing forecasts. | Model ensuring that all stocks and flows are consistently accounted for in the economy over time. |

| Focus | Expectation formation by agents and market efficiency. | Accounting identities between stocks (wealth, debt) and flows (income, investment). |

| Key Assumption | Agents have perfect or near-perfect foresight about economic variables. | Flows affect stocks and vice versa; macroeconomic variables are interlinked through balance sheets. |

| Model Type | Micro-founded, equilibrium-based. | Macro accounting framework, dynamic and realistic. |

| Application | Monetary policy, asset pricing, inflation expectations. | Financial stability, fiscal policy analysis, debt dynamics. |

| Strength | Captures forward-looking behavior and anticipation effects. | Ensures macroeconomic consistency and tracks financial stocks and flows thoroughly. |

| Limitation | Unrealistic assumption of fully rational agents. | Complexity in modeling and requires detailed data on financial stocks and flows. |

Introduction to Rational Expectations

Rational expectations theory assumes that economic agents use all available information efficiently to forecast future variables, leading to unbiased and consistent predictions. This framework contrasts with stock-flow consistency models, which emphasize accounting identities and the interdependence of stocks and flows in the economy. Understanding rational expectations is crucial for analyzing how expectations influence economic decisions and macroeconomic policy effectiveness.

Foundations of Stock-Flow Consistency

Stock-Flow Consistency (SFC) models are grounded in accounting identities ensuring that all flows come from somewhere and go somewhere, preserving monetary coherence across sectors over time. Unlike Rational Expectations models, which assume agents perfectly forecast future variables, SFC emphasizes empirical validation through actual transaction records and stock adjustments, capturing dynamic feedback loops within the economy. The foundational principle of SFC is that every financial asset held by one sector corresponds to a liability of another, ensuring consistency between stocks and flows in macroeconomic analysis.

Core Assumptions: Comparing Both Approaches

Rational expectations theory assumes agents form forecasts using all available information and model-consistent predictions, emphasizing individual optimization and market clearing. Stock-flow consistency focuses on accounting identities and the balance between stocks and flows in an economy, ensuring all transactions are recorded and financial stocks evolve coherently over time. Both approaches contrast in core assumptions: rational expectations prioritize expectations-driven behavior, while stock-flow consistency highlights systemic financial coherence and detailed accounting constraints.

Modeling Economic Agents’ Behavior

Rational expectations models assume economic agents form forecasts based on all available information, aligning their predictions with the actual economic model's outcomes. Stock-flow consistency frameworks emphasize the accounting identities and interactions between stocks and flows, ensuring that agents' behaviors reflect realistic budget constraints and intertemporal financial balances. Integrating both approaches enhances the accuracy of modeling economic agents' behavior by combining forward-looking expectations with robust financial consistency.

Dynamics of Macro Accounting in SFC Models

Rational expectations assume agents forecast future macroeconomic variables using all available information, whereas stock-flow consistency (SFC) models emphasize the interdependence of stocks and flows to maintain accounting identities dynamically. SFC models integrate detailed sectoral balance sheets, ensuring that every flow has a corresponding stock change, which allows for precise tracking of financial stocks and real aggregates over time. This approach captures the complex feedback loops in the economy, providing a more robust framework for analyzing macroeconomic dynamics compared to the forward-looking equilibrium assumptions in rational expectations.

Expectations Formation and Forecasting

Rational expectations theory assumes agents form forecasts by utilizing all available information efficiently, predicting future economic variables without systematic errors. Stock-flow consistency models incorporate endogenous feedback mechanisms where expectations are adjusted based on accounting identities linking stocks and flows, ensuring macroeconomic coherence. This approach emphasizes adaptive expectation formation aligned with observed economic aggregates, enhancing forecasting accuracy in dynamic financial systems.

Treatment of Uncertainty and Shocks

Rational expectations models assume agents form forecasts based on all available information, treating shocks as unpredictable innovations with known probability distributions that agents efficiently incorporate into decision-making. Stock-flow consistency frameworks explicitly model the endogenous feedback effects of shocks within the financial and real sectors, emphasizing the accumulation of stocks and the resulting systemic uncertainty over time. This approach captures the complex dynamics of uncertainty by ensuring that flows and stocks remain consistent, reflecting the realistic adjustments and delayed effects of shocks on the economy.

Policy Implications and Effectiveness

Rational expectations theory assumes agents optimally forecast future policy impacts, often leading to policy ineffectiveness due to anticipated adjustments and market equilibria. Stock-flow consistency models emphasize accounting identities and interactions between stocks and flows, enabling more realistic simulations of policy impacts on aggregate demand, debt dynamics, and financial stability. Policymakers using stock-flow consistent frameworks can design interventions that account for balance sheet constraints and feedback effects, improving the effectiveness of fiscal and monetary policies in stabilizing economies.

Empirical Applications and Evidence

Rational expectations models often face challenges in empirical applications due to their reliance on agents having perfect foresight or unbiased forecasts, which empirical evidence frequently contradicts. Stock-flow consistency (SFC) frameworks provide robust empirical validation by integrating accounting identities and behavioral equations to ensure macroeconomic coherence, enabling more accurate simulations of financial flows and sectoral balances. Empirical studies demonstrate that SFC models better capture real-world economic dynamics, such as debt accumulation and monetary circuit effects, compared to traditional rational expectations models.

Conclusion: Synthesizing Rational Expectations and SFC

Synthesizing Rational Expectations and Stock-Flow Consistency models enhances macroeconomic analysis by integrating forward-looking behavior with detailed accounting of financial stocks and flows. This combined approach improves the accuracy of economic forecasts and policy simulations by ensuring that expectations are grounded in realistic, consistent monetary and fiscal dynamics. Emphasizing the interplay between agents' expectations and the economy's structural constraints provides a more robust framework for understanding economic fluctuations and stability.

Rational expectations Infographic