Inventory turnover measures how efficiently a company sells and replaces its stock within a specific period, indicating the effectiveness of inventory management. High inventory turnover suggests strong sales or effective stock control, while low turnover may point to overstocking or slow-moving goods. Discover how improving your inventory turnover can boost profitability and streamline operations by reading the rest of the article.

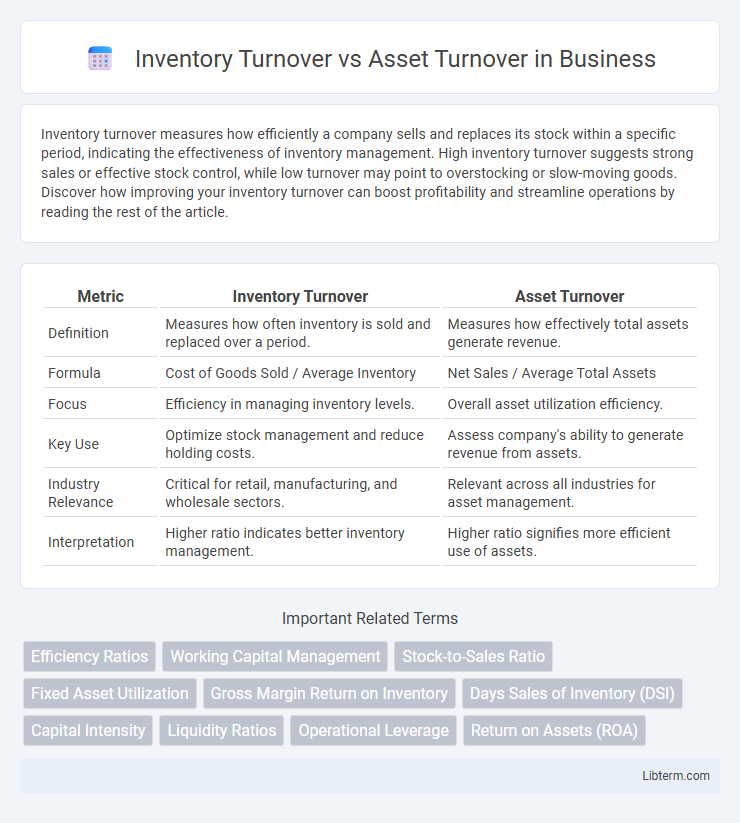

Table of Comparison

| Metric | Inventory Turnover | Asset Turnover |

|---|---|---|

| Definition | Measures how often inventory is sold and replaced over a period. | Measures how effectively total assets generate revenue. |

| Formula | Cost of Goods Sold / Average Inventory | Net Sales / Average Total Assets |

| Focus | Efficiency in managing inventory levels. | Overall asset utilization efficiency. |

| Key Use | Optimize stock management and reduce holding costs. | Assess company's ability to generate revenue from assets. |

| Industry Relevance | Critical for retail, manufacturing, and wholesale sectors. | Relevant across all industries for asset management. |

| Interpretation | Higher ratio indicates better inventory management. | Higher ratio signifies more efficient use of assets. |

Introduction to Inventory Turnover and Asset Turnover

Inventory turnover measures how efficiently a company sells and replaces its stock within a specific period, indicating the liquidity and management of inventory. Asset turnover evaluates how effectively a company uses its total assets to generate sales revenue, reflecting overall operational efficiency. Both metrics offer critical insights into business performance but focus on different aspects of asset utilization.

Defining Inventory Turnover

Inventory turnover measures how efficiently a company sells and replaces its stock within a given period, calculated by dividing the cost of goods sold by average inventory. This metric indicates the liquidity of inventory and helps identify how well a business manages its stock levels relative to sales demand. Unlike asset turnover, which evaluates total asset efficiency in generating revenue, inventory turnover specifically focuses on inventory movement and stock management.

Defining Asset Turnover

Asset turnover measures how efficiently a company uses its total assets to generate sales revenue, calculated by dividing net sales by average total assets. This metric provides insights into management's effectiveness in deploying assets to produce revenue, indicating operational performance. Unlike inventory turnover, which focuses solely on the management of inventory relative to sales, asset turnover encompasses all assets, including fixed and current assets, offering a broader view of resource utilization.

Key Differences Between Inventory Turnover and Asset Turnover

Inventory turnover measures how efficiently a company sells and replaces its stock of goods, calculated by dividing the cost of goods sold by average inventory. Asset turnover evaluates how effectively a company uses its total assets to generate sales, derived from net sales divided by average total assets. The key difference lies in inventory turnover focusing solely on inventory management, while asset turnover provides a broader assessment of overall asset utilization.

Importance of Inventory Turnover in Business

Inventory turnover measures how efficiently a company sells and replaces its stock within a given period, directly impacting cash flow and profitability. A high inventory turnover indicates effective inventory management, reducing holding costs and minimizing obsolescence risk. This metric is crucial for businesses aiming to optimize working capital and respond quickly to market demand.

Importance of Asset Turnover for Financial Performance

Asset turnover measures a company's efficiency in generating sales from its total assets, reflecting operational effectiveness and resource utilization. Higher asset turnover ratios indicate better management of assets to drive revenue, directly influencing profitability and return on investment (ROI). This metric is crucial for investors assessing how well a firm converts investment into sales, impacting long-term financial performance and valuation.

How to Calculate Inventory Turnover and Asset Turnover

Inventory turnover is calculated by dividing the cost of goods sold (COGS) by the average inventory during a specific period, indicating how efficiently inventory is managed. Asset turnover is determined by dividing net sales by average total assets, measuring a company's ability to generate sales from its assets. Both ratios provide critical insights into operational efficiency and asset utilization.

Factors Affecting Inventory and Asset Turnover Ratios

Inventory turnover ratios are influenced by factors such as inventory management efficiency, product demand variability, and supply chain reliability, which affect how quickly inventory is sold and replaced. Asset turnover ratios depend on the company's asset utilization, including the proportion of fixed versus current assets, capital investment strategies, and operational efficiency in generating sales from total assets. Both ratios are impacted by industry norms, technological advancements, and changes in market conditions that alter sales velocity and asset use effectiveness.

Practical Examples: Inventory vs Asset Turnover in Action

Inventory turnover measures how often a company sells and replaces its inventory within a period, such as a retailer selling 8 times per year indicating efficient stock management. Asset turnover reflects how effectively a firm uses all its assets to generate sales, with a manufacturing company generating $2 in sales for every $1 of assets showing strong asset utilization. Comparing both, a grocery store with high inventory turnover but moderate asset turnover highlights rapid product movement but moderate overall asset efficiency, whereas a capital-intensive company like an airline might show low inventory turnover due to minimal inventory but higher asset turnover driven by expensive equipment.

Strategies to Improve Inventory and Asset Turnover Ratios

Implement just-in-time inventory systems to reduce holding costs and increase inventory turnover rates by minimizing excess stock. Enhance asset utilization through regular maintenance and strategic capital investments to maximize productivity and boost asset turnover ratios. Streamline supply chain processes and improve demand forecasting to align inventory levels with sales, thereby optimizing both inventory and asset turnover performance.

Inventory Turnover Infographic