Deferred consideration allows you to structure payment for a transaction over time, improving cash flow and aligning payment with future performance or milestones. This approach can reduce upfront financial pressure and is commonly used in mergers and acquisitions to bridge valuation gaps. Explore the article to understand how deferred consideration can benefit your business deals.

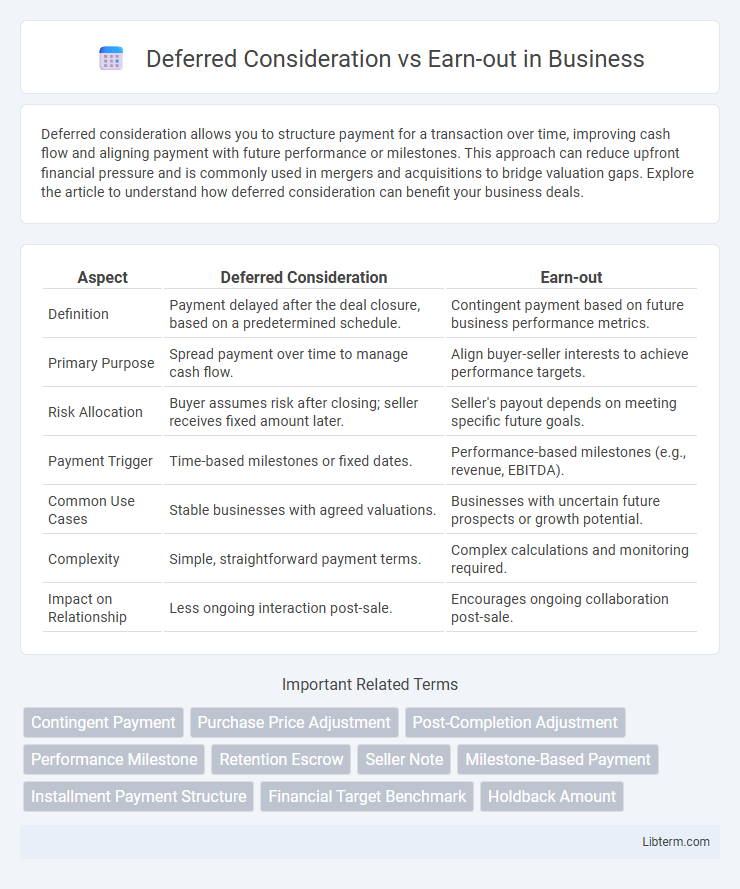

Table of Comparison

| Aspect | Deferred Consideration | Earn-out |

|---|---|---|

| Definition | Payment delayed after the deal closure, based on a predetermined schedule. | Contingent payment based on future business performance metrics. |

| Primary Purpose | Spread payment over time to manage cash flow. | Align buyer-seller interests to achieve performance targets. |

| Risk Allocation | Buyer assumes risk after closing; seller receives fixed amount later. | Seller's payout depends on meeting specific future goals. |

| Payment Trigger | Time-based milestones or fixed dates. | Performance-based milestones (e.g., revenue, EBITDA). |

| Common Use Cases | Stable businesses with agreed valuations. | Businesses with uncertain future prospects or growth potential. |

| Complexity | Simple, straightforward payment terms. | Complex calculations and monitoring required. |

| Impact on Relationship | Less ongoing interaction post-sale. | Encourages ongoing collaboration post-sale. |

Understanding Deferred Consideration

Deferred consideration refers to a payment structure in mergers and acquisitions where a portion of the purchase price is paid at a later date, often based on predetermined milestones or timeframes. This arrangement allows buyers to manage cash flow while ensuring sellers receive full value over time, reducing immediate financial burden. Unlike earn-outs, deferred consideration typically involves fixed payments rather than performance-based adjustments.

What Is an Earn-out?

An earn-out is a financial arrangement in mergers and acquisitions where part of the purchase price is contingent on the target company achieving specific performance milestones post-transaction. It aligns the seller's interests with the company's future success, typically measured through revenue, profit targets, or other key performance indicators over a defined period. Deferred consideration, by contrast, refers to payment delayed to a future date but not necessarily linked to performance metrics, distinguishing earn-outs as performance-based payments within acquisition agreements.

Key Differences Between Deferred Consideration and Earn-outs

Deferred consideration involves a fixed payment schedule agreed upon at the deal's closing, ensuring a predetermined future payment to the seller. Earn-outs are contingent payments based on the business's performance post-transaction, aligning incentives but introducing measurement risks. The key difference lies in deferred consideration's certainty of payment versus earn-outs' performance-based variability.

Advantages of Deferred Consideration for Sellers and Buyers

Deferred consideration benefits sellers by providing guaranteed payment over time, reducing the risk of non-payment and supporting better cash flow management. Buyers advantageously use deferred consideration to preserve immediate capital, easing cash flow constraints and aligning payment obligations with future business performance. This payment structure also minimizes upfront financial risk for buyers while offering sellers secured funds post-transaction.

Pros and Cons of Earn-out Arrangements

Earn-out arrangements offer sellers the opportunity to realize additional compensation based on the future performance of the acquired business, aligning incentives between buyers and sellers. Pros include risk sharing, potential for higher total payout, and maintaining seller motivation for business success post-transaction. Cons encompass complexity in measurement and disputes over performance metrics, potential delays in full payment, and challenges in integration that may impact earn-out targets.

Common Scenarios for Using Deferred Consideration

Deferred consideration is commonly used in mergers and acquisitions when buyers seek to spread payment over time to manage cash flow or align compensation with performance milestones. This payment method is favored in transactions involving private companies where valuation uncertainty exists or when sellers remain involved in operations to ensure smooth transition. In such scenarios, deferred consideration balances risk and reward by linking part of the purchase price to future events without the complexity of earn-out structures.

Structuring Effective Earn-out Agreements

Structuring effective earn-out agreements involves clearly defining performance milestones and financial targets to align the interests of buyers and sellers, ensuring measurable outcomes tied to future payments. Deferred consideration typically sets a fixed payment schedule, whereas earn-outs require detailed clauses on calculation methods, reporting requirements, and dispute resolution to minimize conflicts. Incorporating well-defined timeframes and transparent metrics enhances predictability, optimizes value realization, and mitigates risks inherent in contingent payments.

Risks and Challenges in Deferred Consideration Deals

Deferred consideration in M&A presents risks such as buyer insolvency or underperformance leading to non-payment, creating financial uncertainty for sellers. Valuation disputes and lack of clear payment triggers may result in prolonged negotiations or litigation, increasing transaction costs. Unlike earn-outs, deferred consideration relies heavily on fixed payment schedules, exposing sellers to greater credit risk without performance-based protections.

Legal and Tax Implications

Deferred consideration involves a fixed payment schedule agreed upon at the deal's closing, which simplifies tax planning but may expose parties to risks if future circumstances change. Earn-outs link payments to the business's future performance, creating complex legal agreements to define performance metrics and potential disputes, with tax treatment varying based on timing and structure. Both require thorough legal due diligence and tax advice to optimize liability, enforceability, and regulatory compliance.

Choosing Between Deferred Consideration and Earn-out

Choosing between deferred consideration and earn-out depends on risk allocation and performance alignment in mergers and acquisitions. Deferred consideration involves a fixed future payment, providing certainty but limited incentivization for post-transaction performance, while earn-outs link payment to achieving specific financial or operational milestones, aligning seller and buyer interests. Careful evaluation of deal structure, valuation accuracy, and post-close integration capabilities is critical to select the optimal mechanism for maximizing transaction value and managing potential disputes.

Deferred Consideration Infographic