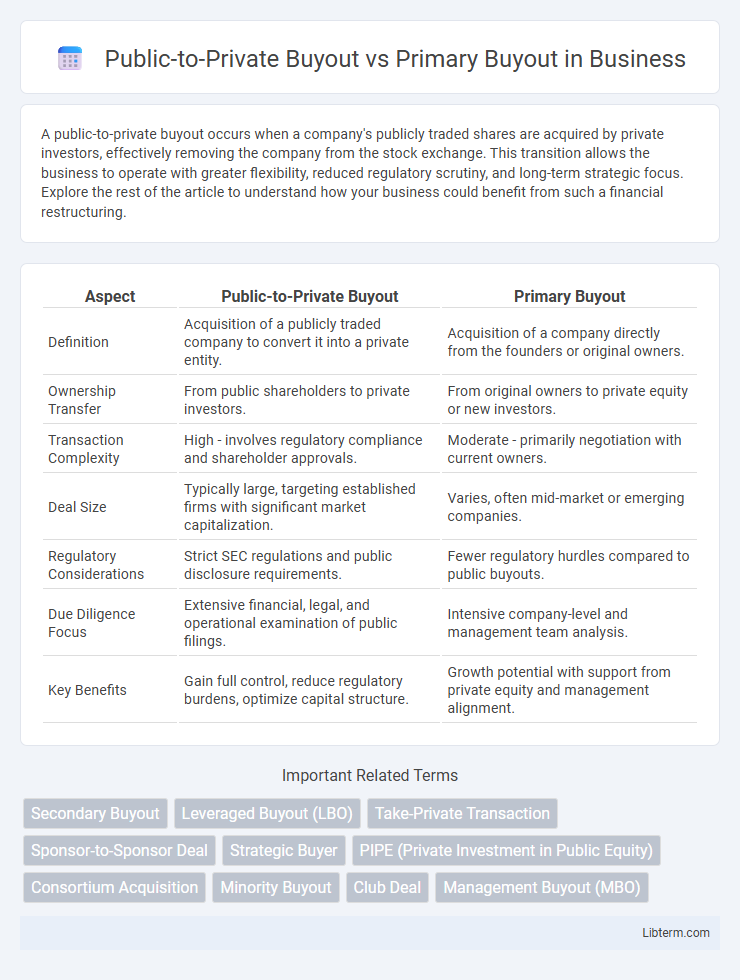

A public-to-private buyout occurs when a company's publicly traded shares are acquired by private investors, effectively removing the company from the stock exchange. This transition allows the business to operate with greater flexibility, reduced regulatory scrutiny, and long-term strategic focus. Explore the rest of the article to understand how your business could benefit from such a financial restructuring.

Table of Comparison

| Aspect | Public-to-Private Buyout | Primary Buyout |

|---|---|---|

| Definition | Acquisition of a publicly traded company to convert it into a private entity. | Acquisition of a company directly from the founders or original owners. |

| Ownership Transfer | From public shareholders to private investors. | From original owners to private equity or new investors. |

| Transaction Complexity | High - involves regulatory compliance and shareholder approvals. | Moderate - primarily negotiation with current owners. |

| Deal Size | Typically large, targeting established firms with significant market capitalization. | Varies, often mid-market or emerging companies. |

| Regulatory Considerations | Strict SEC regulations and public disclosure requirements. | Fewer regulatory hurdles compared to public buyouts. |

| Due Diligence Focus | Extensive financial, legal, and operational examination of public filings. | Intensive company-level and management team analysis. |

| Key Benefits | Gain full control, reduce regulatory burdens, optimize capital structure. | Growth potential with support from private equity and management alignment. |

Introduction to Public-to-Private and Primary Buyouts

Public-to-private buyouts involve acquiring a publicly traded company and converting it into a privately held entity, often to streamline operations and implement strategic changes away from public market pressures. Primary buyouts, on the other hand, entail private equity firms purchasing a company's equity for the first time, typically to drive growth or restructure the business. Both buyout types focus on control acquisition but differ in target company status and investment motivations.

Defining Public-to-Private Buyouts

Public-to-private buyouts involve acquiring a publicly traded company and converting it into a privately held entity, often to enable strategic restructuring away from market pressures and regulatory scrutiny. These transactions typically require purchasing outstanding shares from public shareholders, leading to delisting from stock exchanges. In contrast, primary buyouts usually focus on acquiring companies that are already private or divisions of corporations, emphasizing growth or operational improvements without the complexities of public market transactions.

What is a Primary Buyout?

A primary buyout refers to the acquisition of a company directly from its original owners, such as founders or early investors, often involving private equity firms purchasing a controlling stake. This contrasts with a public-to-private buyout, where a publicly traded company is taken private through the acquisition of its shares. Primary buyouts typically involve growing companies seeking capital and strategic support to expand, rather than the transition from public to private ownership.

Key Differences Between Public-to-Private and Primary Buyouts

Public-to-private buyouts involve acquiring a publicly traded company and taking it private, often requiring complex regulatory approvals and extensive due diligence on publicly available financial data. Primary buyouts target privately held firms, focusing on operational improvements and growth strategies without the need for public market compliance. The key difference lies in the ownership transition and regulatory environment, with public-to-private buyouts dealing with shareholder actions and market disclosure requirements, whereas primary buyouts emphasize value creation within private ownership structures.

Motivations for Public-to-Private Buyouts

Public-to-private buyouts are primarily motivated by the desire to escape the pressures of public market scrutiny, enabling management to implement long-term strategic changes without short-term shareholder demands. These transactions often allow for operational restructuring and cost reductions away from the volatility of stock price fluctuations. In contrast, primary buyouts focus on acquiring a controlling stake in privately held companies, usually to drive growth through capital infusion and strategic guidance.

Drivers Behind Primary Buyouts

Primary buyouts are driven by strategic opportunities to acquire companies with robust growth potential, often utilizing private equity funds targeting undervalued assets. These transactions focus on operational improvements, market expansion, and value creation through active management involvement. In contrast, public-to-private buyouts primarily aim to delist public companies to unlock shareholder value by reducing regulatory burdens and enhancing management control.

Deal Structure and Financing Comparison

Public-to-private buyouts typically involve acquiring a publicly traded company and taking it private, requiring complex financing structures with higher leverage through syndicated loans and high-yield bonds to support large transaction values. Primary buyouts focus on acquiring private companies, often utilizing a mix of equity from private equity firms and debt financing, with structures tailored to the target's existing ownership and cash flow stability. Deal structures in public-to-private buyouts generally demand extensive regulatory compliance and shareholder approval, whereas primary buyouts allow more flexible negotiation between buyers and current private owners.

Risks and Challenges in Each Buyout Type

Public-to-private buyouts face significant regulatory scrutiny and market volatility risks due to the transition from public markets, which can lead to valuation fluctuations and increased financing challenges. Primary buyouts, involving investments in companies with limited financial transparency, bear heightened due diligence risks and operational integration challenges that may affect post-buyout performance. Both buyout types encounter liquidity constraints, but public-to-private deals often grapple with shareholder approval hurdles while primary buyouts deal with sponsor alignment and exit strategy execution risks.

Impact on Stakeholders and the Market

Public-to-private buyouts often lead to significant shifts in shareholder value by removing a company from public markets, impacting liquidity and transparency for public investors but providing management and private equity firms greater control to implement long-term strategies. Primary buyouts, involving the acquisition of a company directly from founders or early investors, typically realign ownership and introduce new capital, enhancing operational efficiency but potentially diluting existing stakeholders' influence. Both buyout types influence market dynamics by altering competitive landscapes, affecting capital flows, and reshaping governance structures, with public-to-private deals causing more pronounced market reaction due to their scale and visibility.

Future Trends in Public-to-Private and Primary Buyouts

Future trends in public-to-private buyouts indicate increased activity driven by low public valuations and a growing appetite for operational improvements away from market pressures. Primary buyouts are expected to benefit from rising institutional investor interest and more robust deal flows fueled by favorable credit conditions and sector-specific growth opportunities. Both buyout types will increasingly leverage technology, ESG considerations, and data analytics to enhance value creation and deal structuring.

Public-to-Private Buyout Infographic