The Law of Supply states that as the price of a good or service increases, producers are willing to supply more of it, and as the price decreases, they supply less. This principle reflects the positive relationship between price and quantity supplied, driven by profit incentives and production costs. Explore this article to understand how the Law of Supply impacts markets and your economic decisions.

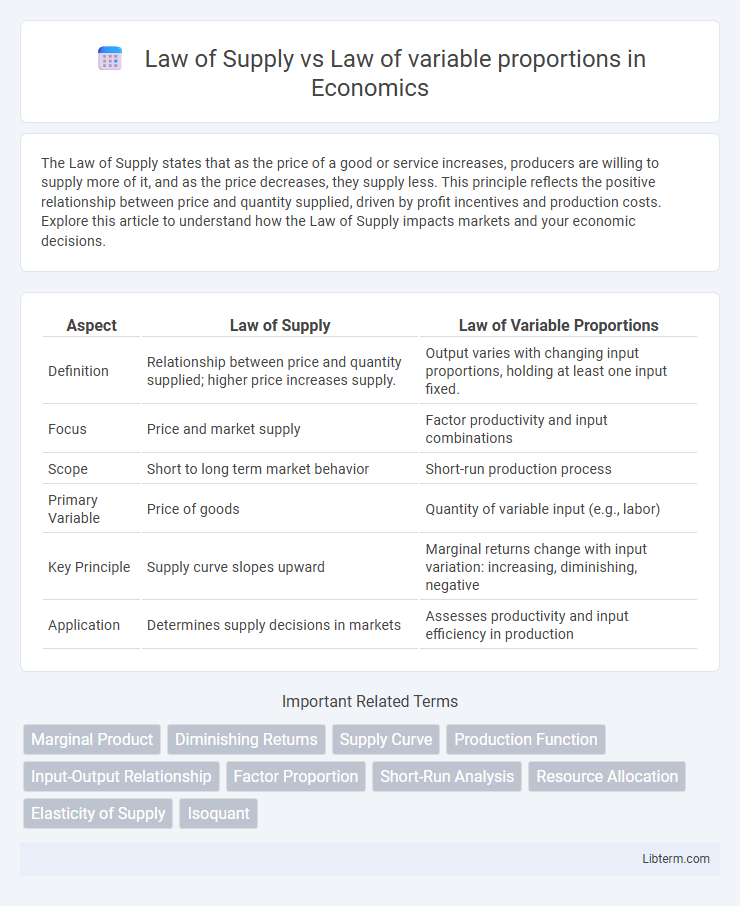

Table of Comparison

| Aspect | Law of Supply | Law of Variable Proportions |

|---|---|---|

| Definition | Relationship between price and quantity supplied; higher price increases supply. | Output varies with changing input proportions, holding at least one input fixed. |

| Focus | Price and market supply | Factor productivity and input combinations |

| Scope | Short to long term market behavior | Short-run production process |

| Primary Variable | Price of goods | Quantity of variable input (e.g., labor) |

| Key Principle | Supply curve slopes upward | Marginal returns change with input variation: increasing, diminishing, negative |

| Application | Determines supply decisions in markets | Assesses productivity and input efficiency in production |

Introduction to Law of Supply and Law of Variable Proportions

The Law of Supply states that, ceteris paribus, an increase in the price of a good results in an increase in the quantity supplied by producers, highlighting a direct relationship between price and supply. The Law of Variable Proportions, also known as the Law of Diminishing Returns, explains how output changes when one input is varied while others are held constant, emphasizing stages of increasing, diminishing, and negative returns. These fundamental economic principles underpin production decisions and market supply dynamics.

Definition of Law of Supply

The Law of Supply states that, ceteris paribus, an increase in price leads to an increase in the quantity supplied, reflecting producers' willingness to supply more at higher prices. This law is fundamental in market economics, illustrating the direct relationship between price and supply quantity. Unlike the Law of Variable Proportions, which explains output changes with varying input proportions, the Law of Supply focuses solely on the price-quantity supply correlation.

Definition of Law of Variable Proportions

The Law of Variable Proportions states that when increasing one input factor while keeping other inputs fixed, the output initially rises at an increasing rate, then at a diminishing rate, and eventually declines. This concept contrasts with the Law of Supply, which describes the direct relationship between price and quantity supplied in a market. Understanding the Law of Variable Proportions is essential for analyzing production efficiency and optimizing input combinations in the short run.

Key Assumptions Underlying Each Law

The Law of Supply assumes that all other factors remain constant, suppliers are rational and aim to maximize profits, and the market conditions are competitive with no external interference. The Law of Variable Proportions presumes that technology is fixed, one input is variable while others remain constant, and the production process exhibits diminishing returns as variable input increases. Both laws rely on the ceteris paribus condition to isolate the impact of key variables on supply and production dynamics.

Graphical Representation and Explanation

The Law of Supply is graphically represented by an upward-sloping supply curve, indicating a direct relationship between price and quantity supplied, where higher prices incentivize producers to supply more. The Law of Variable Proportions is illustrated through a production function curve, typically a concave shape showing increasing output with additional variable inputs up to a point, followed by diminishing returns. Both graphs highlight fundamental economic behaviors: the Law of Supply emphasizes producer response to market prices, while the Law of Variable Proportions demonstrates changes in output based on varying input levels in the short run.

Factors Affecting Law of Supply

Factors affecting the Law of Supply include production costs, technology, prices of related goods, and government policies such as taxes and subsidies. Changes in input prices directly influence the quantity of goods producers are willing to supply at various prices, while improvements in technology can increase supply efficiency. Unlike the Law of Variable Proportions, which focuses on input-output relationships in production, the Law of Supply emphasizes the seller's responsiveness to price changes in the market.

Stages of Law of Variable Proportions

The Law of Variable Proportions, also known as the Law of Diminishing Returns, describes three distinct stages: increasing returns, where marginal product rises as more variable inputs are added; diminishing returns, characterized by a declining marginal product though total output still increases; and negative returns, where additional inputs reduce total output. In contrast, the Law of Supply explains the positive relationship between price and quantity supplied, indicating that higher prices typically incentivize producers to increase output. Understanding the stages in the Law of Variable Proportions is crucial for optimizing input combinations in production processes, unlike the Law of Supply which focuses on market price and quantity supplied dynamics.

Major Differences Between the Two Laws

The Law of Supply explains the direct relationship between price and quantity supplied, stating that an increase in price leads to an increase in supply, holding other factors constant. In contrast, the Law of Variable Proportions focuses on the output changes resulting from varying one input while keeping other inputs fixed, illustrating stages of production such as increasing, diminishing, and negative returns. The former deals with market behavior in response to price changes, while the latter addresses input-output relationships within the production process.

Practical Implications in Economics

The Law of Supply explains how producers increase output as prices rise, guiding firms in setting production levels to meet market demand efficiently. The Law of Variable Proportions focuses on optimizing input combinations in the short run, helping businesses maximize output while minimizing costs when scaling production. Together, these laws assist economists in analyzing production decisions, resource allocation, and market equilibrium in real-world economic scenarios.

Conclusion and Summary

The Law of Supply states that, ceteris paribus, an increase in price leads to an increase in quantity supplied, reflecting producers' willingness to supply more at higher prices. The Law of Variable Proportions explains how output changes when one input is varied while others remain fixed, highlighting stages of increasing, diminishing, and negative returns. Understanding both laws is essential for analyzing production efficiency and market supply dynamics in economics.

Law of Supply Infographic