Direct costs encompass expenses directly tied to the production of goods or services, such as raw materials, labor, and manufacturing supplies. Understanding these costs is crucial for accurate pricing, budgeting, and profitability analysis in your business operations. Explore the article to learn more about how managing direct costs can impact your financial success.

Table of Comparison

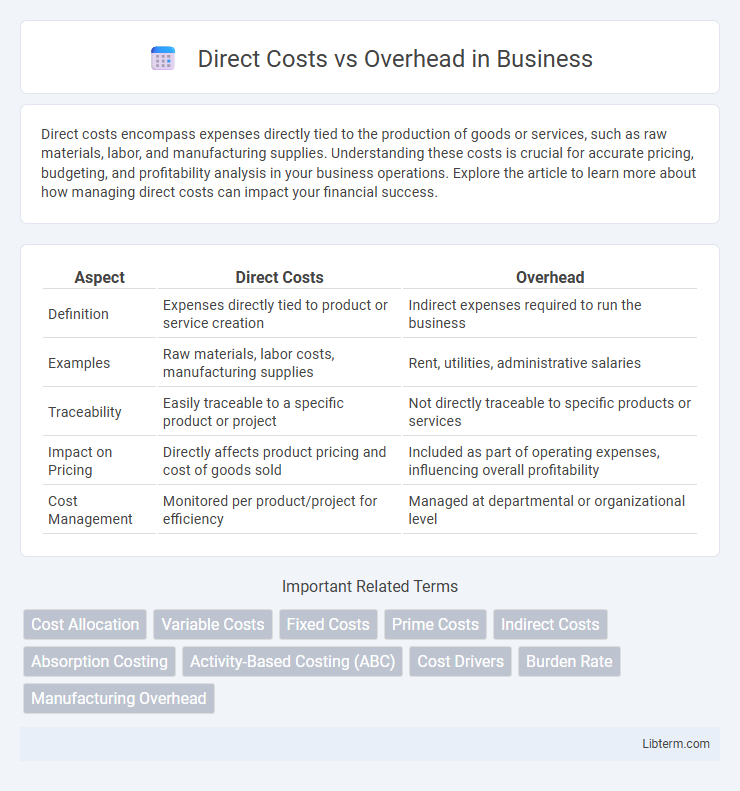

| Aspect | Direct Costs | Overhead |

|---|---|---|

| Definition | Expenses directly tied to product or service creation | Indirect expenses required to run the business |

| Examples | Raw materials, labor costs, manufacturing supplies | Rent, utilities, administrative salaries |

| Traceability | Easily traceable to a specific product or project | Not directly traceable to specific products or services |

| Impact on Pricing | Directly affects product pricing and cost of goods sold | Included as part of operating expenses, influencing overall profitability |

| Cost Management | Monitored per product/project for efficiency | Managed at departmental or organizational level |

Understanding Direct Costs: Definition and Examples

Direct costs are expenses that can be directly traced to the production of a specific good or service, such as raw materials, labor wages for workers on the production line, and manufacturing supplies. These costs are essential for calculating the cost of goods sold (COGS) and play a crucial role in pricing strategies and profitability analysis. Common examples include the cost of steel in automobile manufacturing and the wages of assembly line employees.

What Are Overhead Costs? Key Characteristics

Overhead costs refer to indirect expenses necessary for running a business but not directly tied to a specific product or service, such as rent, utilities, and administrative salaries. These costs are fixed or semi-fixed, recurring regularly regardless of production volume, and essential for maintaining daily operations. Understanding overhead is crucial for accurately allocating expenses and determining true product profitability.

Direct Costs vs Overhead: Core Differences

Direct costs are expenses directly attributable to the production of goods or services, such as raw materials and labor. Overhead costs, also known as indirect costs, include expenses necessary for running the business but not directly tied to production, like rent, utilities, and administrative salaries. The core difference lies in traceability: direct costs can be traced specifically to a product, while overhead costs support overall operations without direct association to specific outputs.

Types of Direct Costs in Business Operations

Direct costs in business operations primarily include raw materials, labor directly involved in production, and manufacturing supplies essential for creating goods or services. These costs are easily traceable to specific products or projects, enabling precise cost allocation and pricing. Examples also encompass equipment usage fees and subcontracted services directly linked to production activities.

Common Overhead Costs: Categories and Examples

Common overhead costs encompass expenses not directly tied to a specific product or service but essential for overall business operations. These categories include rent for office or factory space, utilities such as electricity and water, salaries of administrative staff, and depreciation of equipment. Examples include property taxes, office supplies, and maintenance costs, which are allocated across multiple departments to support indirect activities.

Importance of Accurate Cost Allocation

Accurate cost allocation between direct costs and overhead is essential for precise product pricing and profitability analysis. Misclassification can lead to distorted financial statements and poor strategic decisions, undermining competitive advantage. Implementing robust cost tracking systems ensures that expenses are correctly attributed, enhancing budget control and resource optimization.

Impact on Pricing and Profitability

Direct costs, such as raw materials and labor, directly influence product pricing by forming the base expenses that must be covered to ensure profitability. Overhead costs, including rent, utilities, and administrative expenses, indirectly affect pricing decisions by increasing the overall cost structure, requiring careful allocation to maintain profit margins. Effective management of both direct costs and overhead enables businesses to set competitive prices while maximizing profitability.

Methods for Allocating Overhead Costs

Methods for allocating overhead costs include the traditional costing method, which assigns overhead based on a single cost driver such as direct labor hours or machine hours, and activity-based costing (ABC), which allocates overhead by identifying multiple cost drivers linked to specific activities. Weighted-average and departmental rates are also common approaches, enabling more precise distribution of overhead by reflecting the varying intensity of resource consumption across departments or product lines. Choosing an appropriate allocation method improves cost accuracy, enhances product pricing, and supports better financial decision-making.

Reducing Overhead and Optimizing Direct Costs

Reducing overhead involves identifying non-essential expenses such as excessive administrative costs, utility waste, and redundant processes to streamline operations and improve profitability. Optimizing direct costs requires meticulous tracking of materials, labor, and production expenses to enhance efficiency and minimize waste in the supply chain. Implementing cost control software and leveraging data analytics can significantly improve decision-making and resource allocation for both overhead reduction and direct cost optimization.

Direct Costs and Overhead in Financial Reporting

Direct costs in financial reporting refer to expenses that can be directly traced to a specific cost object, such as raw materials and labor used in production, providing precise attribution of costs for accurate profitability analysis. Overhead encompasses indirect expenses like utilities, rent, and administrative salaries that support overall operations but cannot be directly linked to a single product or service, requiring allocation methods to distribute these costs appropriately. Understanding the distinction between direct costs and overhead ensures accurate financial statements, cost control, and effective budgeting within organizations.

Direct Costs Infographic